Why NY Construction Insurance May Be Toxic To Your Profits

I was having a beer with a friend of mine at a golf outing recently. He’s an accountant in the construction practice group at a major accounting firm. I told him the story about a construction company I met with recently that was underpricing their jobs pretty significantly. For every $1 in contract value they were awarded they are losing over 14 cents. He smiled and told me he sees that all the time. Major companies over expand into markets or trades they don’t fully understand losing their bonding capacity, or worse plain going under. Often it’s a result of not being tight in knowing their true cost of goods and services; construction liability insurance and construction workers compensation insurance being prime culprits.

I will highlight one significant area we see errors; job costing errors due to improper insurance cost allocations. Most construction companies fold insurance costs under their “general conditions” within their construction budgets. If your working in NY it’s a major budgetary component. The challenge is pricing the job at your current insurance cost structure. Contingent on when the job starts that cost structure can change pretty dramatically at renewal, especially in a rising rate environment. If your working on margins of 10 % or less you can easily see how your profits evaporate or worse losses materialize. If the insurance cost increase is high enough you can lose a whole year’s profit in one email. Unfortunately, we see this all too often.

What This Means

“Yeah we get that genius but how can you prevent that?! “ To be clear you can’t prevent it entirely however you can manage the fluctuation to an acceptable level so you can adjust your future pricing to accurately reflect your true costs; here’s how.

Much of what we espouse in terms of risk management has to do with simple protocol and the timing of that protocol. Simply put it’s not just doing “the thing”, but when you do “the thing”. Sort of like closing the barn door BEFORE the horse leaves rather than after….. It’s not simply closing the door, it’s when.

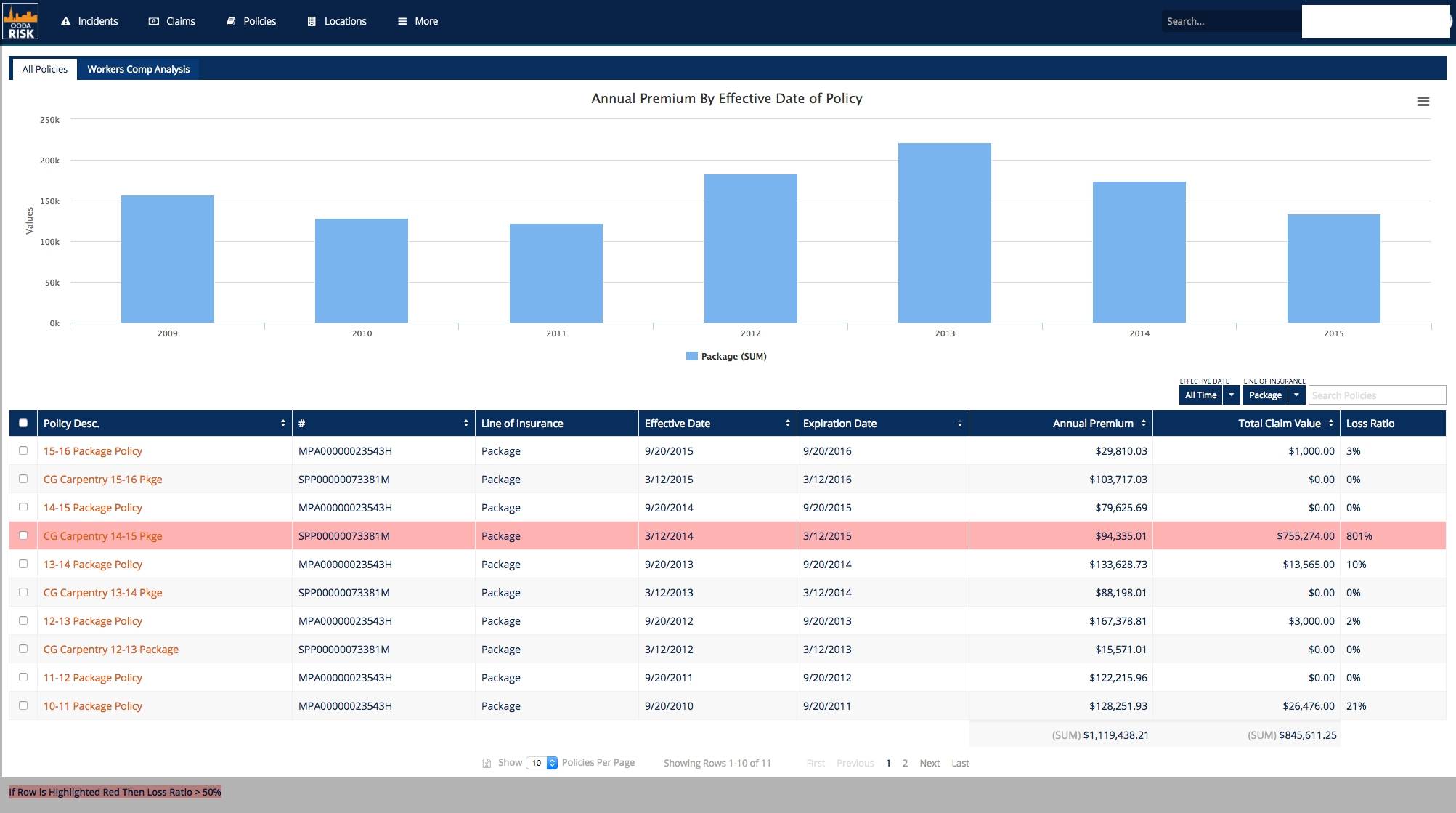

Step 1: Know Your Loss Pic By Line of Insurance:

It’s helpful to understand how the insurance marketplace sees you. Loss Pic is an industry acronym for Loss Picture or Loss Ratio. In simple parlance “how profitable is your account to the insurance company/marketplace ?” The Loss Pic or Loss ratio is a ratio of premiums you have paid in by line of insurance each year to the claims paid out each year. Each insurance product you purchase has a profitability component baked in by the carriers who provide the insurance to you; usually 50%. This means for every $ 1 in premiums the companies will make a profit if they pay 50 cents or less in claims.

Knowing this number for each policy will help you forecast where your insurance rates will be upon renewal. Too few construction companies take advantage of this information early enough as they believe they won’t know their renewal pricing until the line of insurance renews. That’s flawed thinking. We can tell you within 10% standard margin of error where your renewals will be 6 months before you renew simply by knowing your loss ratio or loss pic for each line of insurance. By knowing your 5 year historical loss picture you can tell if the account is profitable to the insurance marketplace or if you’re running a temperature.

Step 2 : When you know the Loss Picture dictates a lot.

At Metropolitan Risk our clients can know their loss picture daily, at any time during the year because of our O.O.D.A. Risk system. Let’s assume you don’t have a Risk Management System. We coach folks to run the loss pic quarterly to see how well your accounts are performing, especially at the 6-month mark (mid renewal). After running the loss pic if you see you’re running a temperature forecast how much of an upward adjustment you might see on your insurance renewal and bake that in to your job costing. Once you sign your contracts you’re locked in on the income side and lack the ability to increase your prices simply because your insurance cost increased. Your G.C. or owner does not want to hear your tale of woe, and woe it is if it’s cheaper for you to stay home and watch Dr. Phil than it is to build.

But, if you have losses running off and expect a decrease, lower your prices and grab market share. The point is you need to start adjusting your RFPs so when you win these future construction contracts you have tighter numbers relative to the actual cost of your construction liability insurance and construction workers compensation costs. If you’re off significantly you’re going to have profitability challenges in your future months as the insurance increase we are seeing are very substantial especially for poor loss histories.

Bottom Line

Bottom line is your insurance policies are NOT something that are managed 1 month before renewal. Best Practice construction firms understand how their construction general liability and construction workers comp claims are developing is a critical function to understand when your organization’s risk-based costs are starting to raise in temperature. Especially in large firms that have lots of activity.

Still have questions? Still want more info? To learn more or speak with a Risk Advisor Click Here to see how you can access your claims and loss pic calcs every day 365 24/7.