For most New York residential owners and operators, independent contractors are just part of doing business. Masonry, roofing, plumbing, unit turns—there’s always another project, another 1099, another COI to track. The problem is that what feels like routine maintenance can quietly snowball into a workers’ comp audit that becomes a major setback in your portfolio’s NOI.

When contractor relationships are loosely managed, the workers’ comp audit becomes the moment where “vendor payments” are reinterpreted as uninsured payroll. Inconsistent contracts, missing or expired COIs, and long-term “1099” staff who function like employees can trigger an expensive reclassification that pushes your premium from a contained line item into a six-figure setback, with an elevated experience mod that lingers for years.

This article walks through, step by step, how that process unfolds for a multi-property operator. The aim is not to alarm you, but to quantify a risk that is often dismissed as paperwork. By standardizing contracts, centralizing contractor records, and building an audit-ready file across every building, you turn contractor management into a strategic control point—protecting margin, preserving valuation, and keeping more of your portfolio’s NOI where it belongs.

Step 1: The Starting Point – Expected Premium on W-2 Payroll

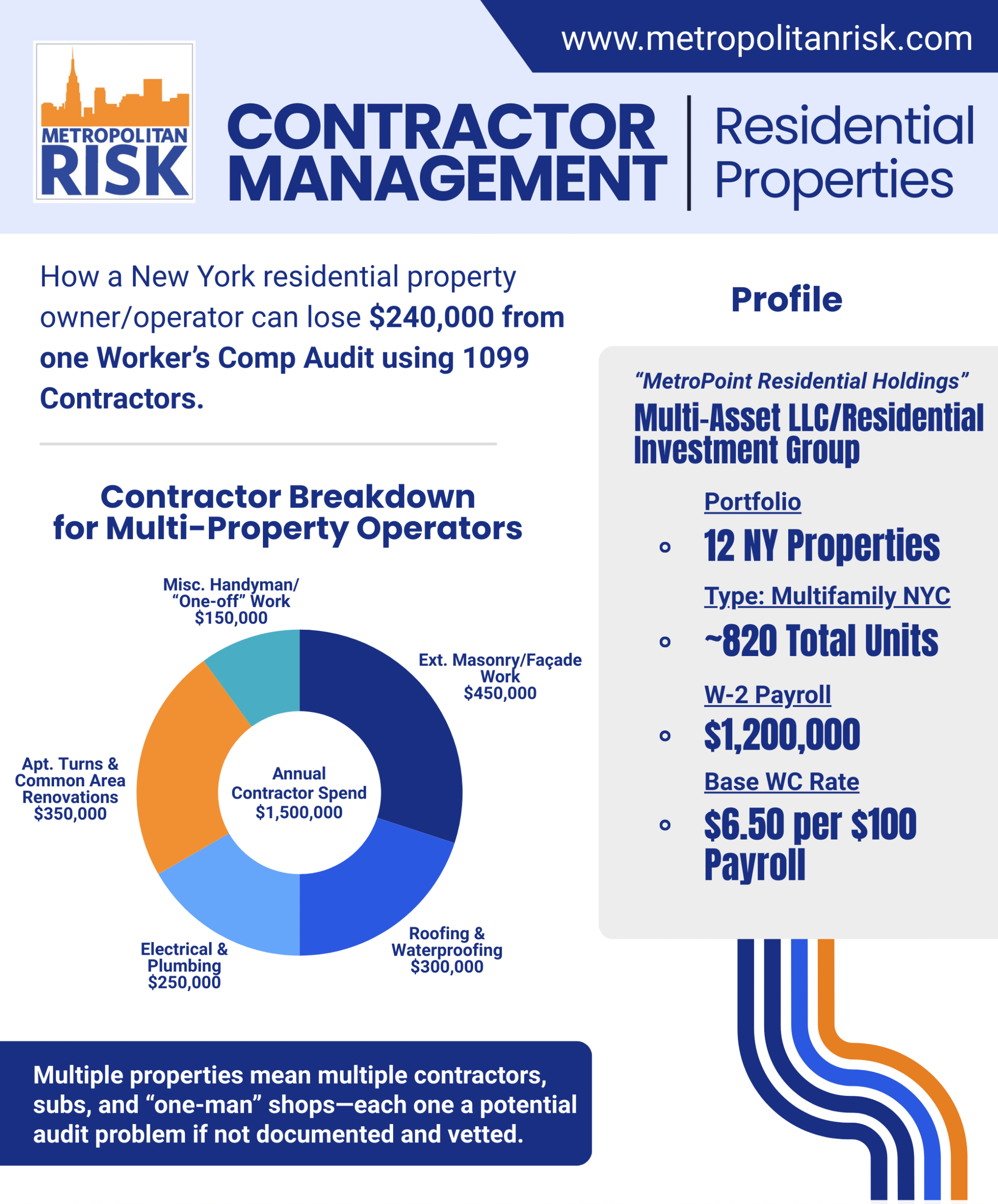

Consider the following operator, MetroPoint Residential Holdings, which owns 12 properties across NYC with roughly 820 units. For the policy year:

- W-2 Payroll (supers, porters, maintenance, office): $1,200,000

- Base WC Rate for Building Operations: $6.50 per $100 of payroll

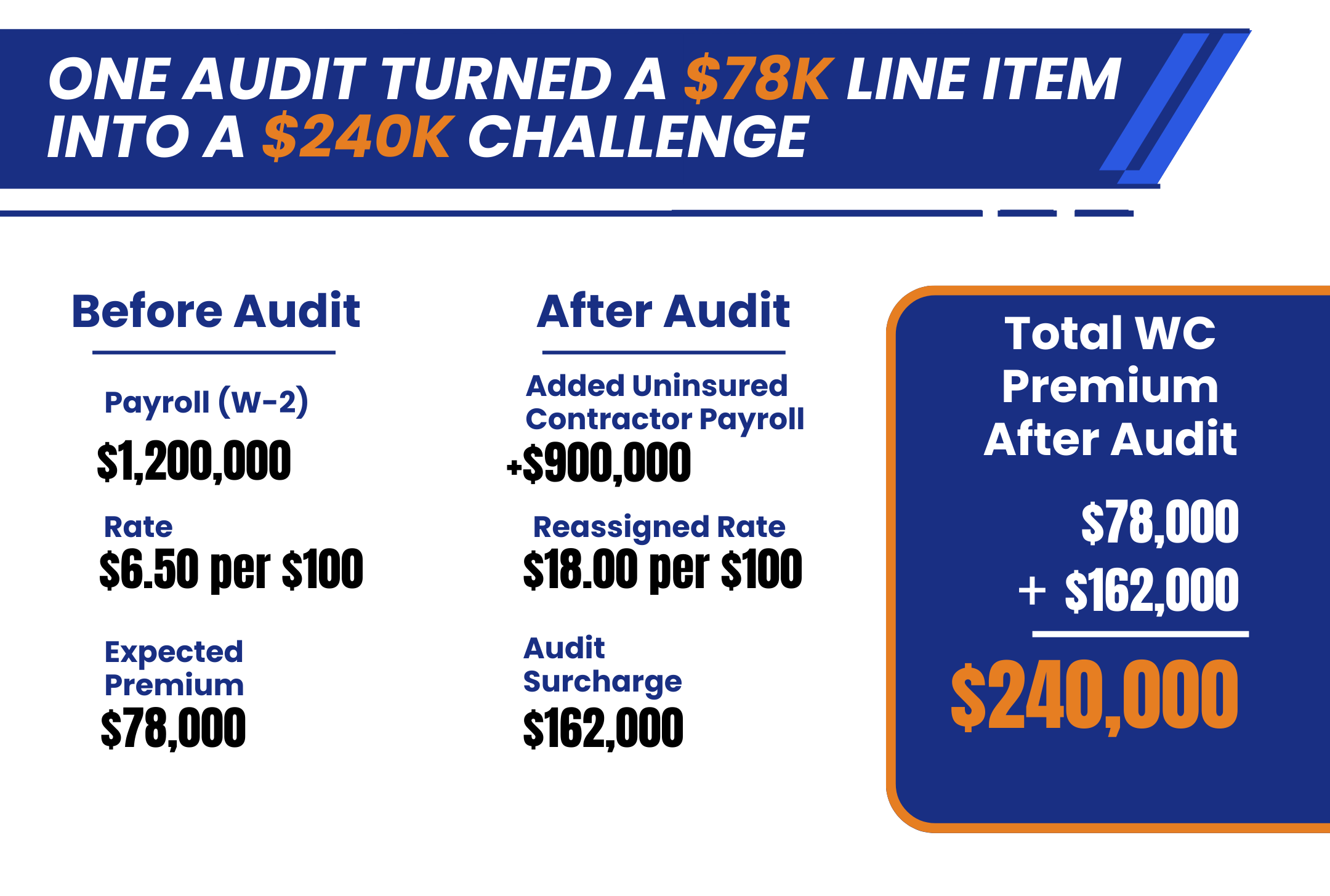

At binding, the carrier estimates premium based on that W-2 payroll alone:

Expected workers’ comp premium

$1,200,000 x 0.065 = $78,000

At this point, everything looks manageable. The WC line item is budgeted, the policy is in force, and operations continue.

Step 2: The Audit Notice – All Payroll & Contractor

After the policy period closes, the carrier initiates a workers’ comp premium audit.

The auditor requests:

- Payroll reports for all W-2 employees

- Detailed records of all payments to 1099 independent contractors

At this point, MetroPoint submits:

- W-2 Payroll: $1,200,000

- 1099 Contractor Payments: $1,500,000

That $1.5M includes masonry, roofing, plumbing, renovations, and small “one-man shop” vendors used across the 12-building portfolio.

Step 3: Documentation Test – Which Contractors Are Off Your WC Books?

The auditor’s next move is straightforward but critical:

“For each contractor, provide a Workers’ Comp certificate of insurance (COI) or a valid exemption.”

This is where process either protects you—or fails you.

Because contractor management is handled inconsistently across properties, MetroPoint can only pull complete, audit-ready documentation for part of the spend:

- Contractors with valid documentation: $600,000

- Contractors with missing, expired, or invalid documentation: $900,000

From the auditor’s perspective, that $900,000 is uninsured labor. Absent proof to the contrary, those dollars are treated as if MetroPoint effectively employed those workers.

Step 4: Reclassification – When Vendor Spend Becomes WC Payroll

The $900,000 in undocumented 1099 payments is now reclassified as MetroPoint’s workers’ comp exposure. Worse, it’s not priced at the relatively modest building operations rate—it’s assigned to higher hazard construction class codes.

For simplicity, assume an average $18.00 per $100 rate for that work:

Audit surcharge on reclassified contractor spend

$900,000 x 0.18 = $162,000

After comparing the before-and-after, one audit has more than tripled the WC spend for that year.

Step 5: The Experience Mod (EMR) – Long Term Impacts

The financial impact doesn’t stop with the audit bill.

Workers’ comp in NY uses an Experience Modification Rate (EMR) that adjusts future premiums based on your historical losses and exposure. A portfolio that appears to be running more payroll in higher-risk class codes—and possibly generating claims from that activity—will often see its EMR rise.

After the audit, MetroPoint’s EMR moves from 1.00 → 1.35:

- Baseline premium: $78,000/year

- With EMR of 1.35:

- $78,000 × 1.35 = $105,300/year

The EMR-driven increase is:

Extra premium per year:

$105,300 – $78,000 = $27,000

If that elevated EMR holds for three policy years, the additional cost is:

Three-Year EMR impact:

$27,300 x 3 = $81,900

Combine the immediate audit surcharge with the future EMR drag:

- Audit surcharge (Year 1): $162,000

- Three-year EMR cost: $81,900

- Total three-year financial impact: ≈ $243,900

That’s nearly a quarter of a million dollars tied directly to how 1099 contractor relationships were documented and managed.

Why This Matters at the Portfolio Level

At the portfolio level, these audit adjustments are far more than an accounting annoyance. When an unexpected six-figure workers’ compensation charge and an elevated experience modification rate are layered onto a 12-property book, they compress NOI, tighten DSCR, and reduce flexibility under loan covenants.

In a competitive market, that detour can be the difference between executing on a growth strategy and standing still. The fundamental issue is not the use of contractors—most residential portfolios will always depend on them. The issue is the absence of a system that keeps contracts, COIs, and audit-ready records consistently aligned across all properties and policy years.

As a result, we’ve assembled a guide for residential owners and operators that lays out a structured approach to contractor vetting, documentation, and audit preparation, so your team can harden its process well before the next policy cycle and keep 1099 payroll reclassification from eroding portfolio performance.