We recently left a meeting with one of the largest construction companies in the country, whose sales are north of a billion dollars annually. The first comment my counterpart made was, “I cannot believe how poor their systems are…” I turned to him and gave him one of my favorite lines because it still rings true to me on a daily basis, “I’m always amazed, never surprised.” Universally, whether you are a billion dollar construction company, a small manufacturer, a non-profit, or a healthcare company, these are the flaws we see in (over 98%) the companies we are invited into. Here are 7 insurance errors commonly made by any and all types of companies.

1. Wrong Goal:

Most companies set a goal of lowering their insurance spending every year. They see it as a tax. It’s an expense that doesn’t generate value. We suggest this goal is incorrect. Your claims history and risk-based costs drive your insurance costs; not your broker or the insurance carriers. 80% of an organizations costs are outside the cost of the insurance. Furthermore, the cost of your insurance program tends to be a lagging indicator, reset only once a year. Measuring, preventing, and managing your claims and claims-related costs should be the goal, not lowering your insurance cost. If you can demonstrate to the insurance marketplace that your company is historically profitable (claims to premium ratio) then you will have carriers competing for your business, which will, in turn, lower your costs.

Wrong Goal

2. Insufficient Resources for the Goal:

The best companies at least have a safety budget. Many, sadly, don’t even have that. If you want your arms around your biggest cost drivers, you need to dedicate resources towards the solution. We suggest that you start by setting a Risk Budget, not just a safety budget. It’s helpful if you know how much money you’re leaking due to claims. Having this Risk/Reward context will help you sell your budget number to management. Moreover, if you have solid systems (see 4), you can leverage those systems to bring in other resources in a cost-efficient fashion. This allows you to stretch the budget.

Most companies don’t leverage their carrier relationships or their brokers for resources to help them with their cost drivers. Even when they do, it’s too inconsistent to have much impact. Staffing at most organizations is thin at best, whereby a single staff person is also delegated the risk responsibilities on top of all the other hats they wear.

![]()

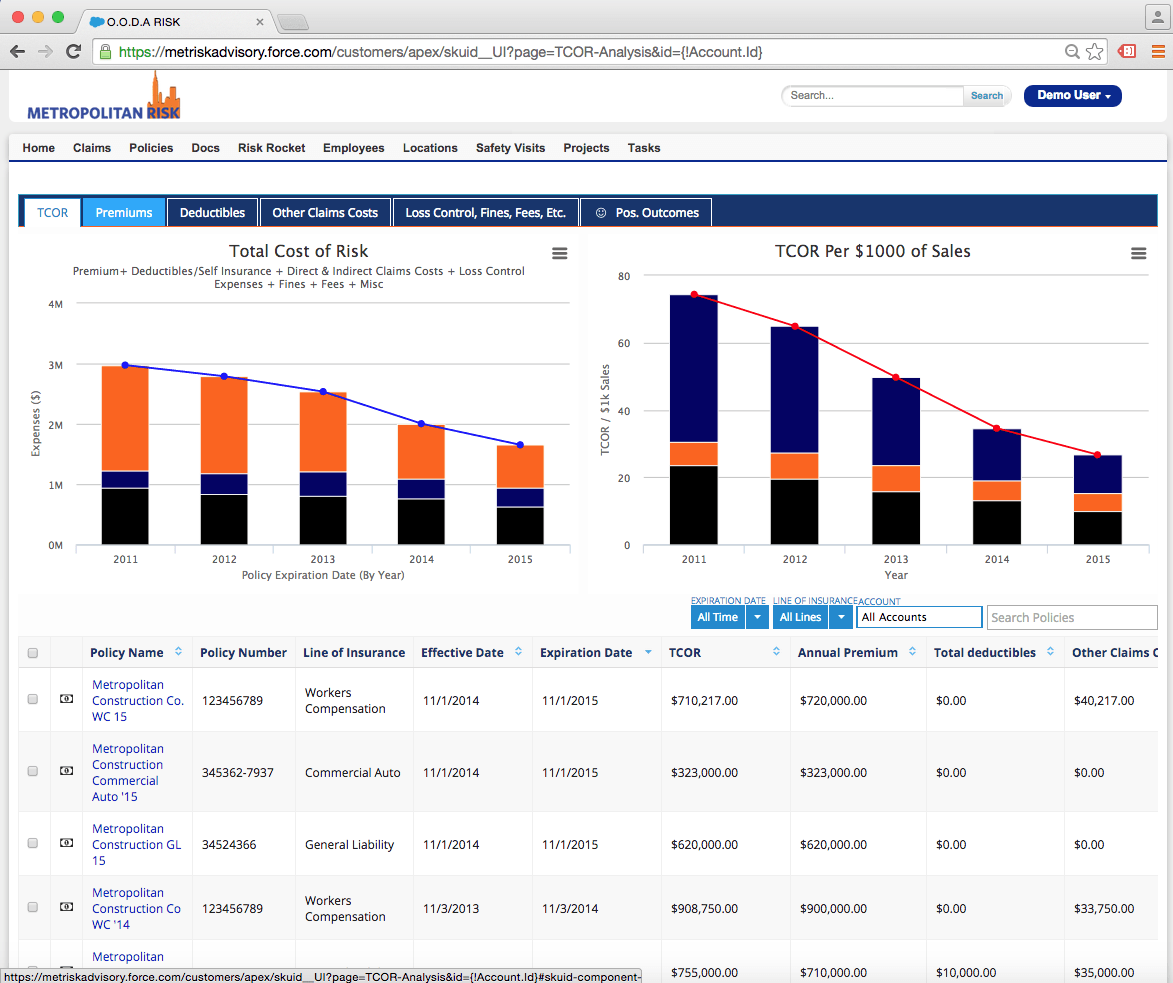

3. Improper to Absolutely No Data:

When we ask prospective clients how they determine success or failure in their insurance program, they almost always tell us insurance premiums. Again, this is flawed. Premiums by themselves indicate nothing and often are also a false read. Instead, premiums should be converted to a rate per sales, payroll, or vehicle. Also, the insurance contracts themselves might exclude or include more risk which swings costs. Our main point is that companies do not have the proper data to reveal their true cost drivers, hot spots, or success spots in an organization. They can’t benchmark themselves over a year’s time. They can’t benchmark supervisory employees, departments, or locations, nor can they tell you what their ROI is on their safety investment. Or they can’t build compensation incentives around the companies cost savings goals.

Without the proper data it’s nearly impossible to change culture, results, or fix cost drivers that you haven’t even identified. Imagine being a doctor trying to diagnose a patient without running tests, looking at charts, and being able to benchmark vitals. Most companies lack this critical ability to gain insight, let alone the ability to select the correct treatment option.

4. Little Strategy:

Here’s a hint, shopping your insurance with 3 competing brokers is not a sound strategy. Yes, it may have worked for you a few times, but, it’s like shooting foul shots backwards. You may get lucky, but it’s not consistently sustainable. If you set the proper goal, you can then test the marketplace with your (1)broker who can (and will) get you competitive pricing. Set your strategy on controlling and lowering your main cost drivers, your insurance costs will follow.

5. Systems:

The best of these companies use spreadsheets to capture data, and then exchange insights via email. Most don’t even have the spreadsheets! If you have a solid system as a nucleus, you can then build both process and staff around this core system. Further you can leverage the system to hire outside specialties to address thorny issues. In absence of a strong core system, it’s very difficult to get a sustained, consistent effort bent towards solving your most vexing claims issues.

6. Lack of Process/Protocol:

There is so much low-hanging fruit that costs so little when it comes to managing claims cost drivers, most of which is just knowing the proper protocol when “x” occurs. Then, it’s all about communicating that protocol organization-wide, with a proper system in place to build in accountability, so it becomes natural.

Note: Having a task list is not a system. Closing the execution loop, holding people accountable, is a system. The loop is closed through a random audit process.

7. Price vs Cost:

This is a big one. Too often, we see companies focus on the price of the insurance against the long term costs. Nothing is more expensive than a cheap insurance contract. You finance your risk with operating cash flows, reserves or worse… loans. Contrary to popular belief the correct answer is not insurance. If you had the correct data, contained within a system, then you would understand the real cost drivers in your organization so you can then attack them strategically. That takes too much work, so folks just look at the premium, write the check and hope for the best.

Here’s the good news (sarcasm). There is a new class of competitor coming to your space that understands these seven points and are executing them with ambitious zeal. They understand that to truly lower their unit cost structure they need to look at their cost of risk rather than the price of their insurance. Having this ability is truly an overwhelming marketplace advantage as they will be cost efficient and cost consistent year in and year out. You will know them by their tale tell signs, high growth, more market share, lower costs and higher profits.

Wash, rinse, repeat.

![]()