As a business leader, you’re accustomed to managing volatile costs—materials, logistics, and labor. But in 2025, the line item creating the most C-suite anxiety is likely your employee health benefits.

The numbers are stark. According to an annual survey from the nonprofit KFF, which provides the broadest picture of U.S. employer health coverage, the average cost for a family health insurance plan has surged to nearly $27,000 this year. This marks a 6% increase from 2024, compounding on top of two previous years of 7% gains.

These cost hikes are not just a line item; they are a strategic problem, rising faster than general inflation and forcing a difficult trade-off between benefits and compensation. This means if healthcare costs rise faster than the economy, there’s less money left over to go to wages.

This isn’t a theoretical problem. For instance, J.H. Berra Paving Co., a St. Louis-based paving company, is grappling with this exact trade-off. They are facing a 15% rate increase this year, on top of last year’s hike. That extra cost is expected to directly cap wage increases for the company’s workers.

For the nearly half of all Americans who receive health coverage through their job, this trend is unsustainable. For their employers, it’s becoming a critical business risk.

What’s Driving the Unexpected Costs?

It’s easy to blame “inflation,” but the drivers are more specific and complex. Understanding them is the first step toward building a resilient strategy.

- Rising Healthcare Spending: The primary driver is simply higher spending on care. Insurers and employers are seeing claims rise due to an increase in chronic conditions, including cancer, among the working-age population.

- Provider Prices: Hospital systems have successfully negotiated higher rates in their contracts, passing those costs directly into your premiums.

- High-Cost Therapies: A major new factor is the explosive growth of new and costly therapies. This category is led by the popular GLP-1 weight-loss drugs, such as Wegovy and Zepbound, which are adding significant, unforeseen costs to employer plans.

This combination of factors has made the insurance market itself more difficult. The chief executive of one Dallas-based wealth-management firm noted that rising spending has made it tougher to shop for coverage, observing “a real tightening among carriers… when it comes to taking on new business”.

The Downstream Impact: A Drain on Time and Talent

The financial cost is only part of the story. For owners and CFOs, the operational burden is immense. That same Dallas CEO, who has around 10 employees, calls navigating the “health-insurance fiasco” a “huge drain” on time that should be spent with clients. For his firm, health insurance is the largest single expense after wages.

To cope with the rising tab, many employers are forced to push more of the burden onto their workers. This often marks the end of long-standing benefits philosophies.

Consider a San Francisco-based architecture firm with roughly 25 employees. For nearly 27 years, the company had covered the full premium costs for its employees. That changed this year after they were hit with a 38% rate increase for their most generous PPO plan.

The founder explained that after years of managing increases through “cuts in other areas, efficiencies and less profits,” they simply “couldn’t absorb it all any longer”. Now, employees must pay extra if they want to keep the generous plan, a difficult but necessary shift.

This story is playing out across the country, often through less obvious means like boosting out-of-pocket charges. Annual deductibles, which had flattened for a few years, have begun ticking upward again, shifting the initial financial risk directly to employees.

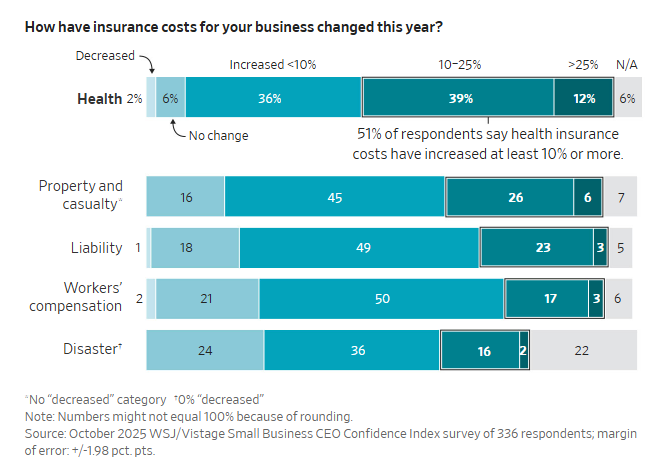

Small Businesses: Facing the Sharpest Increases

While no one is immune, small employers are facing some of the most dramatic rate hikes. A recent survey of 336 small businesses found that more than half reported health-insurance cost increases of 10% or more this year.

The pressure has become so intense that a growing number of smaller employers are moving away from traditional health plans entirely. Recent data signals an “emerging falloff” in the number of small companies providing health benefits at all.

This creates a new risk: losing the war for talent.

Some business owners are turning to creative alternatives. One certified financial planner in South Carolina, who finds traditional insurance a “real nemesis,” now spends 9% of her firm’s gross revenue on medical benefits. Instead of a traditional plan, her company provides health-reimbursement accounts (HRAs) that workers can use to pay for their own premiums.

From Annual Renewal to Year-Round Strategy

If you’re an employer who wants to take care of your people, the current benefits market can feel like an impossible puzzle. The key takeaway is that the old model of simply “shopping your plan” once a year is no longer effective.

The answer isn’t in a simple spreadsheet comparison. It’s in a year-round, data-driven approach. This means:

-

analyzing your specific claims data to understand if your costs are being driven by pharmacy (like new GLP-1s) or by hospital network contracts

-

exploring alternative funding models—like level-funding or defined-contribution HRAs

-

finding a pharmacy benefit manager (PBM) who works for you, or pairing a high-deductible plan with an employer-funded HSA

Finally, it’s about communicating that value. When employees understand why the PPO plan costs so much and how to be a better healthcare consumer, everyone wins. This strategic approach stops the painful, annual trade-off between benefits and wages, turning your health plan from your biggest liability into a powerful tool for retention and growth.