WHAT is Assigned Risk?

WHAT is Assigned Risk?

Most states require companies to effectuate a workers compensation policy in order to legally run their business. However, carriers can decide not to insure certain companies because of the risks associated with a company’s industry, poor claims history, and/or other workers compensation related factors. Every state offers some type of program that guarantees workers compensation coverage for all companies that cannot obtain coverage directly from the insurance carrier of their choosing. For New Jersey, the NJWCIP can assign certain insurance carriers to cover these undesirable companies through their “Assigned Risk Plan.” Every company in New Jersey that is eligible and applies to the Assigned Risk Plan is guaranteed a workers’ compensation policy. However, along with not having much control over the policy that is chosen for them, companies who are forced in to applying for Assigned Risk can be assessed an additional surcharge of anywhere from 15 to 35% of their premium. In other words, your company wants to avoid Assigned Risk!

WHY You Should GET OUT of the Assigned Risk Plan?

Companies that apply for the Assigned Risk Plan, or “Market of Last Resort,” typically have high risks and will therefore experience high insurance premiums. Assigned Risk’s additional surcharge is calculated as a percentage of your premium payment(after your mod surcharge). So with a high premium, and high mod, this surcharge will have an even higher impact on your costs. The following chart shows some rough examples of premiums with corresponding surcharges that an Assigned Risk carrier can charge your company. This surcharge should be recognized as a loss because it can simply be avoided with proper risk management.

*In this simplified example, consider annual premium as the final amount you would pay, including your experience modification surcharge. For a more detailed example, scroll down.

Think of Assigned Risk’s cost to your company in the long run. If you are paying an insurance premium of $250,000, you can lose $87,500 every year just from being classified under the Assigned Risk Plan. This cost can accumulate and in just 4 years you will have unnecessarily paid $350,000. Start the process of getting your company off of the Assigned Risk Plan and you will save hundreds of thousands of dollars.

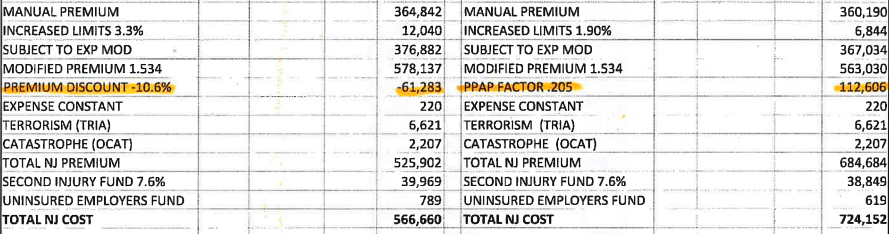

Here is an example of someone who got a quote inside Assigned Risk & outside. You will notice a few things. One, in Assigned Risk they were assessed a 20% surcharge (PPAP Factor). In their quote outside of Assigned Risk not only do they avoid that $112,000+ surcharge but they get a $61,000 premium discount (companies in Assigned Risk are not eligible.) The final result? Roughly $160,000 per year savings! The other thing you will note however is that 1.5 experience mod adding a $200,000 surcharge. While focusing on getting out of assigned risk is important, lowering that mod is where the true long term savings will occur. The combination of a lower mod, and removal from Assigned Risk, could easily save this mid-size company $350,000-$400,000/year. But that is for another article. If you’d like more information on how to do so, contact us about our Comp Care program.

HOW To GET OUT of Assigned Risk?

You are in Assigned Risk because your business has issues in the eyes of the insurance carrier and therefore you are not attractive to them. The proper way to go about getting out is to know WHY you have these issues and taking a long term approach towards fixing them. Sit down with your insurance broker to come up with a solid strategy to make you more attractive to them. Once that approach is in place, it is your broker’s job to market you to the carrier. Just the fact that you are taking the APPROPRIATE action in engaging a risk management program can help, as opposed to shopping your policy to attempt to fix your issues. That is called treating the symptom, while you really want to cure the disease. For example going to a B rated carrier is not a long term solution and it also will not fix your experience mod problems.

The most prevalent reasons for being in Assigned Risk are:

- Poor Claims History

- Certain High Risk Industries

- Small or New Business

Some issues are easier than others to fix. But they are all curable. For your claims issue, you need to start by having an impact on safety & culture to prevent them from happening in the first place. Maybe you will want to invest in loss control. You should also have a trusted partner on the back end as well. Your insurance partner should be pressuring liability and workers comp adjusters to factually substantiate their reserving practices, and to close out files and claims fast as these claims have a a large impact on your renewal. This is a practice that is continuous 52 weeks a year and not simply done at “renewal time” as it’s too late by then.

If you’re a new business it helps to show the carrier a resume that proves you have experience in the industry or running a business in general. If you’re in a high risk industry, there are in fact carriers that will write your business, but it is no doubt harder. They do it on a case by case basis and it helps to have a broker who has a deep knowledge of workers compensation, your business, and a great relationship with workers comp carriers that write your class of business.

The Assigned Risk Plan provides a valuable product and fills a need in the world of workers comp insurance. But for most employers a trip into the pool is not a pleasant one. For a plan and/or guidance on how your specific company can get off of or avoid the Assigned Risk Plan and save capital in both the short and long run, please call a Risk Advisor at 914-357-8444. We will provide a free consultation and analysis.