A common cause for New York workers compensationinsurance claims can be overexertion. In fact, the Bureau of Labor Statistics recently published 2017-2018 overexertion statistics. They found that 295,000 in 2017 and 282,000 overexertion injuries in 2018 caused days off from work, and naturally, WC claims. These take up 31% of the non-fatal; work injuries that cause work days lost. This could result from a wide range of activities, such as lifting, carrying, throwing, pushing, or pulling. Although it is easy to overexert muscles, there are a few simple tips you could give your employees to help prevent such injuries. These near 600,000 days lost are all preventable by doing simple daily routines differently. Here are a few of these examples.

Start Easy

Many people have a tendency try to do too much when first starting a project. The result is that they end up injuring themselves, which means their work has to be put on hold until they heal.

Pace Yourself

Some make it a point to work as fast as possible. Unfortunately, they do not seem to realize that they could easily injure themselves while working at such a quick pace.

Know Your Limits

Regardless of the activity that a person is doing, it is always a good thing to know when to ask for help. Many people injure themselves by overdoing an activity, such as lifting a box that is clearly too large for one individual.

Set Obtainable Goals

Many times a person sets goals that he or she has no hope of actually reaching. By being reasonable with their workload, employees reduce the risk of injuries while still earning a sense of accomplishment.

Overexertion could happen regardless of how physically fit a worker is. This is why it is important to train your employees in the proper way to perform their job functions. Otherwise, you may be facing a New York workers compensation insurance claim and staff shortages.

Over a decade ago in May of 2008, a Crane collapsed in NYC that killed 2 construction workers. The Wall Street Journal and the New York Times both profiled the company owner Mr. James Lomma of NY Crane & Equipment Corp and the assistant district attorney, Eli Cherasky spoke on the matter saying “They were killed because a wealthy man was concerned about the bottom line and nothing else.”

We’re still talking about this accident today because of the effect it had on one construction business. Your safety policies may not be the strongest because you believe that this will not happen to your business. Like all risks, there is the possibility this could happen to you, but you have the opportunity to learn from someone else’s expensive mistake.

5 Critical Tips On Avoiding a Very Expensive Education On Safety:

Hire a site safety coordinator. Senior management and your new site safety coordinator need to have a concise safety plan that needs to be implemented company-wide.

Budget for committed resources for safety in every new project. Safety does pay a dividend although many don’t bother to understand or calculate it.

Offer a team bonus if your team achieves certain safety goals and enforce penalties for violations. You win as a team and you lose as a team while on a worksite.

Start every project by reviewing your previous numbers and creating new safety goals based on past experiences. Learn from your past mistakes instead of making the same ones.

Call in a professional. A professional may cost money, but an accident or claim could put you out of business.

If you understand the cost of loss, insurance claim or injury to your profit margins then it is much easier to commit a fraction of those management resources to safety. Its not just good business, it is the right thing to do for your community and your employees.

Are you ready to implement a plan but don’t know where to start? Request A 5 Minute Call with one of our Risk Advisors at no cost 1.914.357.8444

Commercial Insurance is one of those things that every company has but not every company understands. In some cases, a person is chosen to be put in charge of the insurance buying process and this person is usually an HR person who has a very little understanding of what goes into the insurance buying process.

To recap the video, commercial insurance is essentially when a person, business, or group of people transfer a risk that could cost money in damages to an insurance carrier. To transfer the risk, the business will pay a flat fee – a premium – that changes in cost every year based on the previous year’s claims. There are also difference types of insurance as well, including workers compensation for worker injuries on the job. There is also auto liability, general liability, property damages, and others.

The one part of insurance many do not understand is: Why do carriers agree to this? The damages may be 10x the insurance premium. It turns out that out of the hundreds of millions of premium policies carriers write every year, they will lose money on only a very small fraction of them. When insureds (those buying insurance) pool their risk into a small group of carriers, many of them pay for a premium. However, much of the time it turns out that their were no damages or claims to need compensation. That does not mean they should not pay for insurance the next year. Insurance is for the protection against the unpredictable. A driver with a perfectly clean record can skid on ice one day. Those damages can cost tens of thousands of dollars.

Learn about the different types of commercial insurance and the role it plays inside of your business. This is just a starting point to learn some of the basics of commercial insurance.

Still have questions? Call one of our risk advisors today at 914-357-8444. Or, visit our website here.

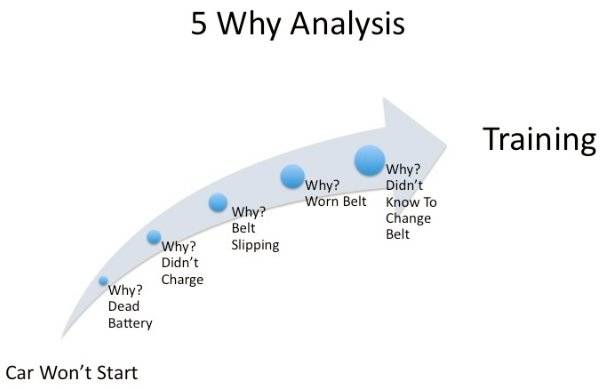

Remember when your kids annoyed you by responding to everything you said with “Why?” Well, there was a genius to that tactic only children can impart. The 5-Why Analysis is a method used to determine and understand the root cause of a problem by repeating the question “why?” five times. Each answer forms the basis of the next question.

There are no hard and fast rules about what questions to explore, or how long to continue the search for additional root causes (e.g. asking “why?” seven or eight times instead). Therefore, the outcome of the analysis will always depend upon the knowledge and persistence of the people involved.

Here is a relatively simple example of Why Analysis:

Problem: The car will not start!

Why? – The battery is dead. (First why)

Why? – The alternator is not functioning. (Second why)

Why? – The alternator belt has broken. (Third why)

Why? – The alternator belt was well beyond its useful service life and not replaced. (Fourth why)

Why? – The vehicle was not maintained according to the recommended service schedule. (Fifth why, a root cause)

Just as annoying children so often do, it would be easy to continue asking “why?” in order to delve even deeper into the problem. However, five repetitions will generally suffice in leading to a root cause.

About Why Analysis

It is important to note that the determined root cause should almost always point toward a process that is not working well or does not exist, rather than something simple and generally uncontrollable such as “There wasn’t enough time.” Answers that are out of our control are not helpful; further in most cases what you will discover in your 5 Why Root Cause Analysis is a failure of process, which is the ultimate goal. You can’t manage and improve what you don’t know.

The developer of the 5-Why Analysis method Sakichi Toyoda was head of the Toyota Motor Corp who used this method to great effect. Toyoda has some helpful tips and strategies to think about when performing “ Why Analysis”:

Use paper or whiteboard instead of computers

Writing the issue helps you formalize the problem and describe it completely. It also helps a team focus on the same problem

Look for the cause step by step. Don’t jump to conclusions.

Base our statements on facts and knowledge; not conjecture.

A root cause should never be something as simple as “human error” or “workers’ inattention”

The Why Analysis can be used in day to day business life, and is especially helpful when dealing with persistent problems that never seem to go away. Stubborn and recurrent problems are often so because they contain deeper issues, and “quick fixes” only solve the surface issues.

Need help dissecting and solving a recurring problem safety or employee injury problem? Don’t hesitate to call us at (914) 357-8444. We have been invited into thousands of businesses to break down their challenges and help solve for “x” , usually high insurance costs driven by claims. We will help you get to the why that much quicker. Time is money, gives us a call.

Why NY Construction Insurance May Be Toxic To Your Profits

I was having a beer with a friend of mine at a golf outing recently. He’s an accountant in the construction practice group at a major accounting firm. I told him the story about a construction company I met with recently that was underpricing their jobs pretty significantly. For every $1 in contract value they were awarded they are losing over 14 cents. He smiled and told me he sees that all the time. Major companies over expand into markets or trades they don’t fully understand losing their bonding capacity, or worse plain going under. Often it’s a result of not being tight in knowing their true cost of goods and services; construction liability insurance and construction workers compensation insurance being prime culprits.

I will highlight one significant area we see errors; job costing errors due to improper insurance cost allocations. Most construction companies fold insurance costs under their “general conditions” within their construction budgets. If your working in NY it’s a major budgetary component. The challenge is pricing the job at your current insurance cost structure. Contingent on when the job starts that cost structure can change pretty dramatically at renewal, especially in a rising rate environment. If your working on margins of 10 % or less you can easily see how your profits evaporate or worse losses materialize. If the insurance cost increase is high enough you can lose a whole year’s profit in one email. Unfortunately, we see this all too often.

What This Means

“Yeah we get that genius but how can you prevent that?! “ To be clear you can’t prevent it entirely however you can manage the fluctuation to an acceptable level so you can adjust your future pricing to accurately reflect your true costs; here’s how.

Much of what we espouse in terms of risk management has to do with simple protocol and the timing of that protocol. Simply put it’s not just doing “the thing”, but when you do “the thing”. Sort of like closing the barn door BEFORE the horse leaves rather than after….. It’s not simply closing the door, it’s when.

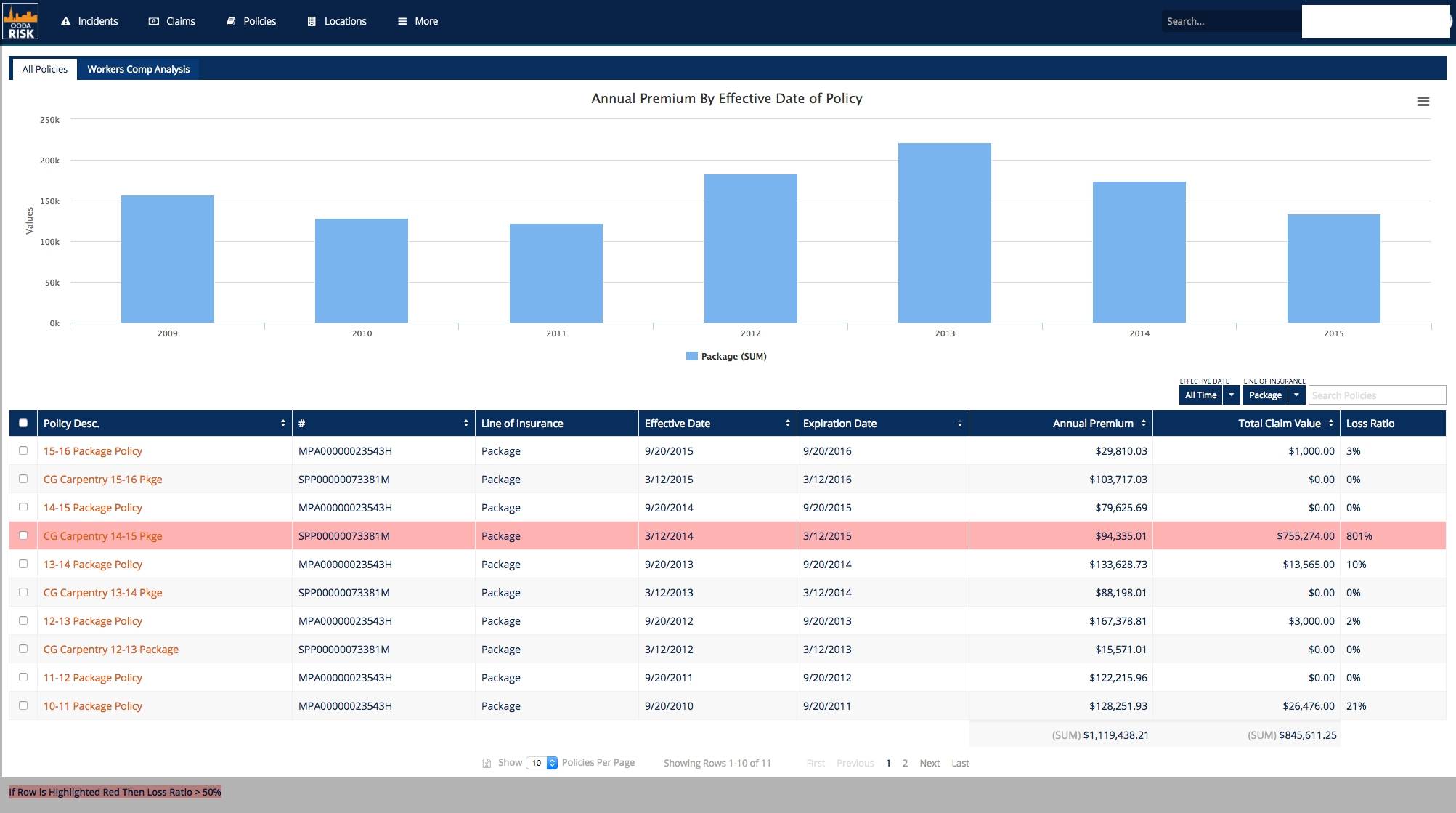

Step 1:Know Your Loss Pic By Line of Insurance:

It’s helpful to understand how the insurance marketplace sees you. Loss Pic is an industry acronym for Loss Picture or Loss Ratio. In simple parlance “how profitable is your account to the insurance company/marketplace ?” The Loss Pic or Loss ratio is a ratio of premiums you have paid in by line of insurance each year to the claims paid out each year. Each insurance product you purchase has a profitability component baked in by the carriers who provide the insurance to you; usually 50%. This means for every $ 1 in premiums the companies will make a profit if they pay 50 cents or less in claims.

Knowing this number for each policy will help you forecast where your insurance rates will be upon renewal. Too few construction companies take advantage of this information early enough as they believe they won’t know their renewal pricing until the line of insurance renews. That’s flawed thinking. We can tell you within 10% standard margin of error where your renewals will be 6 months before you renew simply by knowing your loss ratio or loss pic for each line of insurance. By knowing your 5 year historical loss picture you can tell if the account is profitable to the insurance marketplace or if you’re running a temperature.

Step 2 :When you know the Loss Picture dictates a lot.

At Metropolitan Risk our clients can know their loss picture daily, at any time during the year because of our O.O.D.A. Risk system. Let’s assume you don’t have a Risk Management System. We coach folks to run the loss pic quarterly to see how well your accounts are performing, especially at the 6-month mark (mid renewal). After running the loss pic if you see you’re running a temperature forecast how much of an upward adjustment you might see on your insurance renewal and bake that in to your job costing. Once you sign your contracts you’re locked in on the income side and lack the ability to increase your prices simply because your insurance cost increased. Your G.C. or owner does not want to hear your tale of woe, and woe it is if it’s cheaper for you to stay home and watch Dr. Phil than it is to build.

But, if you have losses running off and expect a decrease, lower your prices and grab market share. The point is you need to start adjusting your RFPs so when you win these future construction contracts you have tighter numbers relative to the actual cost of your construction liability insurance and construction workers compensation costs. If you’re off significantly you’re going to have profitability challenges in your future months as the insurance increase we are seeing are very substantial especially for poor loss histories.

Bottom Line

Bottom line is your insurance policies are NOT something that are managed 1 month before renewal. Best Practice construction firms understand how their construction general liability and construction workers comp claims are developing is a critical function to understand when your organization’s risk-based costs are starting to raise in temperature. Especially in large firms that have lots of activity.

Still have questions? Still want more info? To learn more or speak with a Risk Advisor Click Here to see how you can access your claims and loss pic calcs every day 365 24/7.

If you are like most small to mid-sized organizations (under $1 billion in sales) then you should be prepared to define these two terms and understand their consequences for your business.

Risk Financing is a fancy term for insurance. Think equities instead of stock. Insurance, in its basic form, is the mechanism whereby an individual or company (Buffalo Wild Wings) packages their risk (fire, injury to public or employee) and sells it to an insurance carrier for a premium.

The theory is that if the insurance carriers’ risk selection process (this is called underwriting) is tight, then the carriers will make a profit by paying less in claims than the premiums they take in from your company. This is their ultimate goal, and it’s referred to as underwriting profit. As their losses deteriorate or your losses deteriorate, they raise rates to offset it. This maintains that profit equilibrium that they always seek. Thus, the premiums they charge you are a function of your claims history and theirs, which results in the costs to finance your risk.

A company usually will finance different branches of risk with different carriers who may have a particular niche or specialty. Add up all those premiums and that is your basic cost of risk. As your losses increase, your costs increase. Are we good so far?

Cost of Risk is similar to above with one notable exception: It includes many more risk variables and cost components that are contained in your Profit & Loss Statement that are much less obvious.

Let’s take, as an example, an accident that occurred with a delivery truck for a large shipping company. This is on my mind as I recently had a few beers with a friend who is a supervisor for this national shipping business. A driver pulling up on a four way intersection looked down briefly and slammed into the back of a school bus, injuring the driver, several children and a pedestrian walking in front of the school bus. Yeah, that’s a nightmare if you’re the supervisor or owner of a small company who does not have the resources to handle it.

Here are some additional components that are usually indirect and ambiguous, but should be included in a typical cost of risk calculation:

Liability insurance surcharges, due to the large auto liability claim that will be filed by the parents and bus company. Did you really think your renewal was going to be flat?

Liability insurance surcharge for the payout to the injured pedestrian. Cha-ching!

Lost productivity of the injured shift worker.

Cost of packages delayed, not delivered.

Cost of additional shift worker needed to take over the route from the injured driver.

Cost of repair for the damaged vehicle.

Increased workers’ compensation cost due to injured worker.

Management and Administrative cost of handling the loss internally at the company. Ever spend a whole day in court or deposition?

Contingent on how granular you want to get, I think we made our point. There are so many indirect costs outside the cost of risk financing (insurance) that need to be accounted for if you really want to have an idea on how to manage or change your costs. The aforementioned variables will be contingent on what you do and how you do it. At this particular company, they did an excellent job tracking all of these floating items, which helps them really keep tight control on their unit cost structure. This is critical in a commodity business.

Conclusions & Takeaways

Companies that understand that their Cost of Risk Financing is really driven by their Cost of Risk Components have in place systems to identify their pain points and cost drivers so they can benchmark and improve them, which in turn lowers their unit cost structure. The strong management they implement makes them beasts to compete with in their native markets.

Furthermore, because they are tracking their cost of risk continually throughout the year they have a firm handle on what their ultimate insurance costs will be very early on. Companies that just track their insurance premiums are too late to the game; insurance premiums are poor lagging indicators. By the time you get your renewal, your costs have already escalated. Had you been tracking your cost of risk variables you would have known early on, and hopefully taken measures to improve your hot spots.

You can’t manage what you don’t know. We here at Metropolitan Risk contend that if you can’t measure it, you can’t manage it. If you can’t manage it, then your cost structure is very, very vulnerable to events that may have enormous impact on your ability to be competitive within your industry.

In our data driven economy those organizations that understand the difference between Cost of Risk and Cost of Risk Financing will have a system like O.O.D.A. Risk to begin to manage their cost drivers and use that data to measure, benchmark and attain results instead of outcomes.

Do you ever wonder how successful people consistently achieve their goals? Have you unlocked why you achieve certain goals while others fall short? Do you want to transform goals to achievements?

Many companies start the new year with new goals and aspirations, some of the most common being:

Reduce Costs

Retain Clients

Increase Profits

Improve Employee Safety

Improve Employee Morale

The most common mistake companies make in outlining such objectives, however, is not providing enough details and specifics. This ambiguity is often at the root of most failed goals, but it is not the cause. Most of us have heard of “writing down” our goals or cutting out pictures of the visions of our successes and making a “collage” and posting it, where we can see it every day and remind ourselves of where we want to go. This practice may seem impressive, but it doesn’t ensure that we will be successful because we haven’t focused on the most important factor . . . HUMAN NATURE!

As Chip and Dan Heath wrote in their book Switch, when significant change is involved in accomplishing your goals, you must appeal to both sides of the brain:

Emotional

Rational

AND, you must influence all three of these areas:

Environment

Heart

Mind

Most of the changes we’re referring to require a significant adjustment in behavior. If you don’t allow for this, you are doomed to fail, and HUMAN NATURE is such that it resists these changes. An example would be the common goal of weight loss. Anyone can eat just fruit and veggies for one or two meals and maybe even one or two days, but eventually the sheer willpower needed to continue on this path will wear off and “poof” there goes that plan! What’s essential for success is appealing to these two sides of the brain: Emotional and Rational. The Rational side tells us it makes “sense” to do something. The Emotional side ACTUALLY does it.

A few years ago I met John, a client, and he was in the midst of dealing with a major challenge in his business. John had maintained a successful plumbing business that he started by himself when he was just seventeen years old. From humble beginnings, John found something he was good at and kept doing it. As the years went by, he added one employee at a time, and before he turned around, he had more than eighty people working for him, and sales exceeding $10 million per year! The problem was that John was working at least eighteen hours a day and constantly chasing many aspects of his business. John’s company completely lacked efficient systems and a cohesive structure, and while he was “successful,” he was also “exhausted.” He knew that this pace was unsustainable. Something had to change or he would have health problems or have to sell the business. John finally turned to taking on a partner, Anthony, to run the “accounting and operational” sides of the business, which was certainly a step in the right direction. It was just the beginning, however, for he had only dealt with one of the areas necessary for significant change: Mind. In fact, he never changed the environment. All his employees and culture remained the same, and he also never changed his heart. He saw his new partner as a “magic bullet.” John continued to do business and manage his operations exactly the same way. His attitudes and operating behavior never changed and, accordingly, Anthony was constantly putting out fires and looking backward at what wasn’t working and what was wrong, and never had a chance to build to the future and restructure. Ultimately, John was defeating his own partner and goals because he wasn’t fully committed to change.

Without appealing to BOTH sides, when the going gets tough, the “emotional side” will get going and leave all “rational” thought behind by falling back into the habits that feel comfortable.

The 3 Essential Keys to transform goals to achievements :

Specifically direct the Rational part of the brain by scripting the initial steps in the new work process along with a clearly outlined step-by-step process (a decision tree of sorts).

Then motivate the Emotional part of the brain by being specific in the GOAL and what the goal LOOKS and FEELS like. Doing this will empower the emotional side of the brain when the tough and challenging times come. And they will come! You need to realize that the challenges and almost “failures” will happen, but be aware that they are not “failures”—rather, they represent the education that is needed to perfect these changes.

Shape the path that will direct the team through the challenges along the way and what guiding principles are needed to stay on track.

All in all:

The START is scripted. The GOAL is specific on how it will feel and look. The path between START and GOAL is impossible to know completely, so you must have your guiding principles in place and stay on the PATH.

I spend most of my time helping companies deal with a very common challenge —employee injuries and the claims associated with them. This problem is even more common for such industries as construction, manufacturing, healthcare, and transportation, where the simple act of opening their doors to do business involves an innate “risk” associated with practically every aspect of their work. These companies certainly don’t want their employees to get hurt, nor do they want the added expense that goes along with paying for the medical care and lost wages associated with these injuries. If I were to merely indicate how much it’s costing them, I would only be appealing to the Rational side of their brain. Conversely, if I were to only explain that these injured employees have families, I would only be stating the obvious—no one wants to hurt someone’s family. I would only be appealing to the Emotional sIde of their brain. At Metropolitan Risk, we use a series of analytics to determine:

What is currently happening and identifying any trends—FACTS

What it’s costing you—RATIONAL

What opportunity/opportunities are available to you to handle these issues—EMOTIONAL

What you need to do—ACTION PLAN & LEADERSHIP = SHAPE THE PATH

As fall approaches each year, it triggers our strategic thinking about our company goals for the next year and how we will achieve them as an organization. I am sure if you are taking valuable time to read this, you also have the foresight to plan, budget, and execute a Profit & Loss Statement.

Most businesses that operate today compete primarily on their unit cost structure. Their adjusted gross profit is the difference between the cost of goods and services and the delivered price for the product or service. The lower your unit cost structure, the higher your profit margin—or the more competitive your price or service—allowing you to grow market share.

Simple concept, yet we still find an unrelenting focus on top-line growth (sales/revenue) coupled with penny-wise, dollar-foolish cost cutting. Generally, the companies that consistently dominate their respective marketplaces do so by strategically cutting costs and investing in strategies that ultimately lower their cost of doing business long term.

In over 23 years of consulting with businesses of all sizes, one of the most common mistakes we have seen is the perspective that insurance is a costly expense that is only managed by shopping around to get the best price. If you are one of these folks, you are not alone, as this is how the overwhelming majority of businesses attack their insurance conundrum. That’s actually great news for you.

As the New Year approaches, our suggestion is to look at insurance as a smaller component of an overall risk reduction strategy that will substantially lower costs across your Profit & Loss (“P&L”) Statement, year in and year out. What number would you rather have—a 10 percent reduction in your insurance premium, which fluctuates up and down each year, or a consistent, sustainable three points in your profit margin?

In today’s evolving marketplace, many best practice firms are leveraging their vendor partners for extra services, driving extra value to their organization. The insurance brokerage relationship is one of the primary areas these firms are mining in order to drive down their unit costs and gain a competitive advantage.

Listed below are a few examples of the services these companies are leveraging through their insurance brokerage relationship.

Three services you should look to take off your plate next time you’re in the market for a new insurance broker.