CCIP or OCIP Workers Compensation claims can cost you a lot.

Contractor Controlled Insurance Program (CCIP) and Owner Controlled Insurance Program (OCIP) are insurance programs that are designed to “wrap up” most, if not all, all of the insurance needs for a project and generally include general liability insurance, workers compensation insurance, builder’s risk insurance and excess or umbrella insurance coverage as well. The owner or general contractor of the OCIP / CCIP purchases workers compensation for all enrolled contractors; relieving them the responsibility of purchasing and providing coverage on the sub contractors workers compensation policy. The insurance company issues a “master” policy to the OCIP / CCIP owner. Each individual sub contractor is assigned an individual policy number. Think of it like a mother with children. The “mother” has the master policy and all of the “children” or sub-contractors, have an individual policy number.

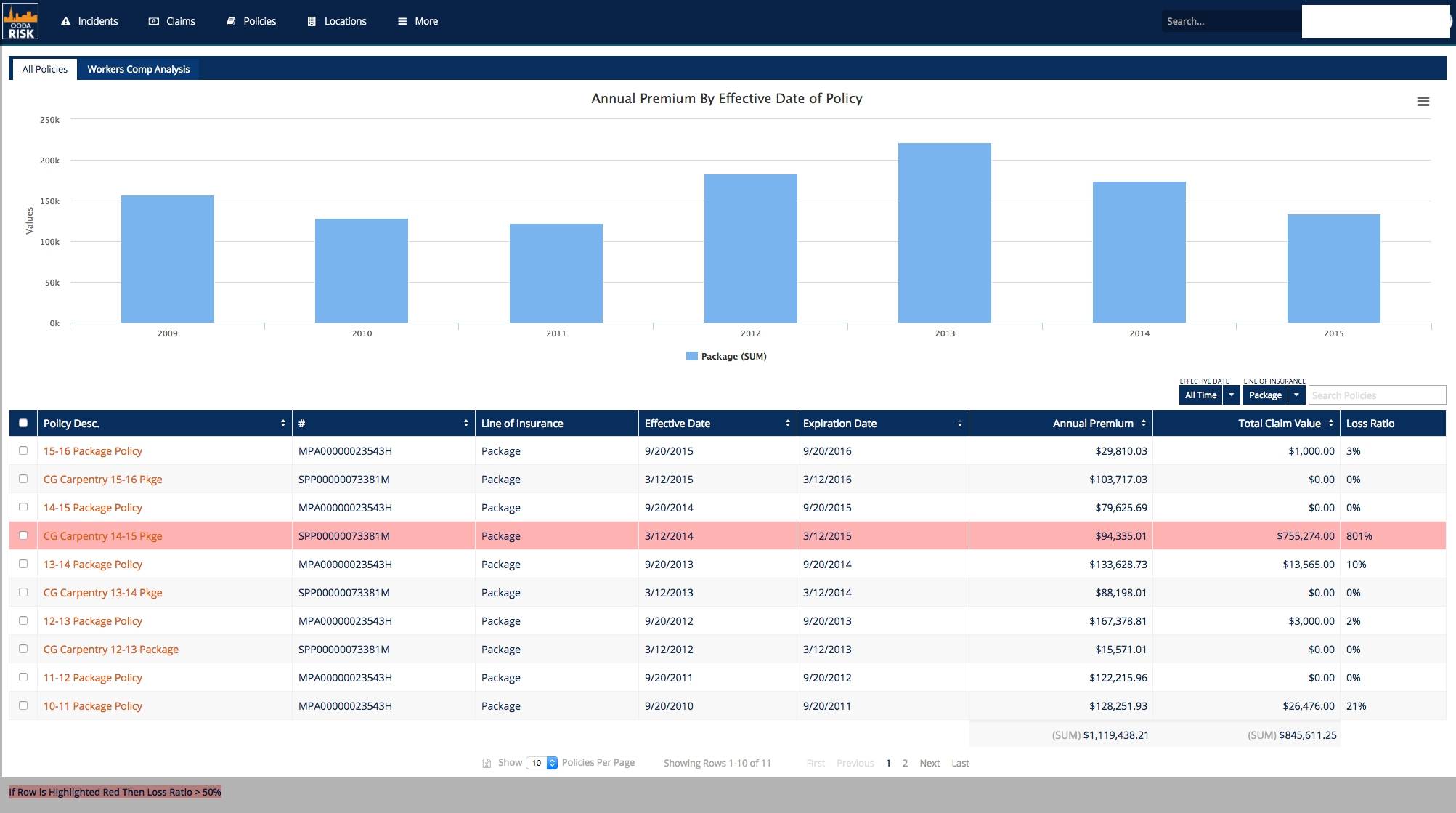

When claims arise, somebody sends the individual contractor’s policy a code. This allows the loss experience to follow the contractor, not the OCIP / CCIP owner. Claims occurring on an OCIP/CCIP project will impact your EMR the same way as claims occurring on non-OCIP work. For this reason, you still need claims management on these claims.

For those who don’t understand the impact of the EMR:

Assigned to your company is an EMR stands for Experience Modification Rating. This tells the state, potential clients,

OCIP owner’s insurance company or third-party administrator manages workers’ compensation claims arising out of an OCIP project.

The claim handler gives primary consideration to the OCIP owner and ignores the fact that the individual contractor is also an insured. For this reason we strongly recommend contractors continue to apply their own internal BEST PRACTICE reporting procedures so they can track and maintain their own records internally as these employee injury claims will still impact your organization. Best practice claims procedures were designed to ensure critical information is gathered early on and documented which allows the claims to settle faster and a much lower payout. The longer the delay in reporting the claim, the higher the payout. The payout can increase as high as 40% or more.

By managing claims in a similar way we encourage them to be, this will lessen the financial impact on both the employee and the business. We encourage you to have a point person within your organization who is tasked with closing out every open claim if you are not doing so already.

Reporting, monitoring, and closing out all of your employee injury claims.

These are key takeaways respective of OCIP / CCIP programs your company may be enrolled in.

This is irrespective of who is actually writing the claims check. The worker’s comp claims report to the Wrap administrator and will follow your company in the form of the EMR. Your state’s workers’ compensation rating board or the NCCI (National Council of Compensation Insurance) gives you this.

This drives the ultimate cost of your worker’s compensation insurance premiums in the form of either surcharges or credits. If your EMR exceeds 1.2 you may not be eligible to bid on certain federal contracts which has an “opportunity cost.” Some General Contractors may set a maximum allowable EMR of 1.0. No sub-contractor with above a 1.0 can bid on future work with that GC.

CLICK HERE to download our FREE GUIDE.

You keep building, we will keep helping you manage your risk so you can win future work.

If you found this helpful please share on social media so we can keep producing quality content to help your business remain cost efficient, cost consistent.

{kind=link}

{kind=link}