You’ve just seen your Experience Modification Rating (EMR) and it is high again. Or your worst-case scenario, it has gone up again. Year over year, you’ve spent time shopping for your insurance due to your high EMR. It is time to stop shopping and start proactively working to lowering your EMR because eventually, it will catch up to you.

What Is Your Experience Mod?

Let’s start with a basic definition. What is your Experience Modification Rating or your EMR? A simple definition of EMR is Payroll divided by Claims. The video below explains what your experience mod is and what is expected of your organization. (If the video does not play in your browser click here.)

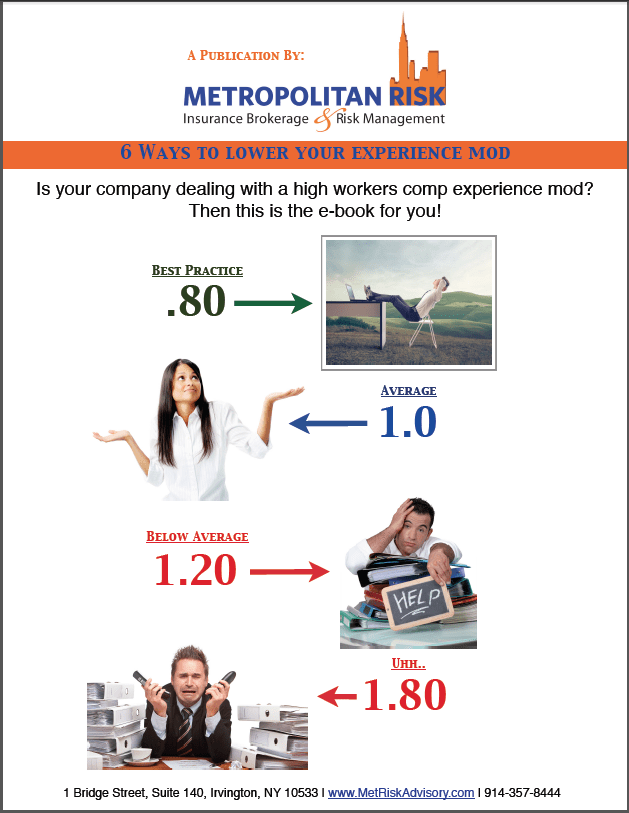

Remember, an average experience mod is a 1.0, this is like receiving a “C” on your report card. If you’re happy with this, stop reading now. Good luck, you’ll be competing against companies with a greater competitive advantage than you because they’ll have a much lower cost structure, higher profits, and a larger business development budget.

Some Construction companies bidding on government work are ineligible if their EMR is above 1.0.

How To Find Your Experience Mod Rate

The NCCI (National Council on Compensation Insurance), is a group that calculates Experience Modification Factors for companies across the entire United States. Some states have their own rating bureaus due to their size and complexity. For example, New York and New Jersey have the NYCIRB & NJCRIB respectively. For a detailed explanation of what your Experience Modification Factor is and how it’s calculated visit this site.

Why is Your Experience Mod High?

There are a number of reasons why your EMR is high. The biggest factor is the number of open claims. If your organization has a high number of claims or one large claim on your Workers’ Comp policy your EMR may stay high until that claim is closed.

How This Affects Your Organization

What this means is that most companies will see another increase in their Experience Modification Factor following their next recalculation. That takes place on their “Unit Stat Date,” and, if left unchecked, your business could face higher rates, possible penalties, and Labor Department Violations.

What You Can Do To Lower Your Experience Mod:

- Track incidents (near misses) not just claims. Most claims can be avoided if you are meticulous about tracking all of the near misses that lead up to the eventual incident. Most claims could have been avoided in hindsight as the employee typically was taking shortcuts long before the ultimate injury occurred. Track these infractions and you will prevent at least one injury a year.

High Experience Mod

- Investigate accidents immediately and thoroughly; take corrective action to eliminate the hazard. If you sense fraud, get aggressive; don’t be an easy target. We suggest Why Analysis follow all incidents. That’s a whole other article that can be accessed HERE.

- Report all incidents to your insurance broker or Risk Advisor immediately. Studies show the longer it takes to report a claim, the more expensive it will be. A 4-week delay in reporting an injury drives the cost of that same injury by 48% according to a Hartford Insurance study of over 2 million claims.

- Alert your workers’ compensation claims adjuster to any serious, potentially serious or suspect claims. Frequently monitor the status of the claim, and communicate with the adjuster to resolve them as quickly as possible. Too busy to do that, have our Claims Advocates communicate with the adjuster on your behalf. Our Claims Advocates were insurance adjusters so they speak that language holding the carrier’s adjusters accountable.

- Every reported claim to your insurance carrier no matter the line of insurance should have an action plan attached to it to close out the claim. This is a big mistake most businesses make. They report it and then forget it until the policy comes up for renewal. At that point, they are shocked at the increase in the workers’ compensation insurance premium which is always driven by claims experience. Folks forget that workers’ compensation insurance is really a very expensive credit line to the business.

- Take an aggressive approach to providing light-duty or transitional to all injured employees upon their release from treatment. Return To Work programs are extremely powerful tools for lowering the cost of a workers’ compensation claim as they give leverage back to the employer, stopping the tail from wagging the dog. Supervise light duty employees to ensure their conformance with restrictions.

- In serious cases that involve lost time, communicate with the claims adjuster to demonstrate your interest in returning the injured employee back to gainful employment.

- Set safety performance goals for those with supervisory responsibility. Success in achieving safety goals should be used as one measure during performance appraisals. At Metropolitan Risk this is just one of the K.R.I’s (Key Risk Indicators) we emphasize to establish internal standards and accountability.

- Develop a written safety program, and train employees in their responsibilities for safety. OSHA rules dictate for every facility location or job site there must be a competent person. Incorporate a disciplinary policy into the program that holds employees accountable for breaking rules or rewards them for correctly following safety procedures. This should be tied into the employee handbook which each employee receives when they are on-boarded for your org.

- Frequently communicate with employees, both formally and informally, regarding the importance of safety keeping safety top of mind at all times.

- Make safety a priority – senior management must be visible in the safety effort and must support the initiative.

- Evaluate accident history and near-misses at least monthly. Look for trends in experience, and take corrective action on the worst problems first.

- Ensure your payroll and class codes are accurate. Over 65 % of workers’ compensation audits have errors. See COMP CHECK .

- Ensure the correctness of your mod calculation. Far too often there are errors here as well. See COMP CHECK

You can build all this out organically by yourself OR speak to a Risk Advisor about our COMP CARE PLATFORM. We have this all built. It’s turn-key and ready to be deployed in your organization if you are serious about reducing your workers’ compensation costs. There are no short cuts…

How Metropolitan Risk Can Help

Still looking for more info? Still have question? We have a team of Risk Management specialists who are here to help! Contact a Risk Advisor today for more information on how you can work towards lower workers comp costs by closing claims instead of shopping for insurance. Click here to book a 5-minute call with a Risk Advisor