Over the years we have seen, the mistakes home healthcare agencies make when they purchase their home healthcare agency liability insurance, their professional liability insurance for home healthcare, agencies and workers compensation to protect their home healthcare aides. It’s critical that you choose an insurance brokerage firm that specializes in the home healthcare agency space so that you can leverage their collective wisdom. Don’t let your education become too expensive.

With profit margins as thin as they are within Home Healthcare Agencies #1 uncovered liability claim could be fatal to even the best run Home Healthcare Agencies. One area we see many other insurance brokers get wrong when they design the liability insurance program for home healthcare agencies is the professional liability exposure centered around patient transfers.

Moving patients around for bathing, sleeping, and general care is a foundational function for home health aides. You would think that if you purchased a liability insurance program for your home healthcare agency that the patient transfer exposure would be covered, especially for the premiums they charge. Spoiler alert, often times it does NOT.

QUICK NOTE : Insurance carriers understand that neither you the end buyer of the home healthcare agency liability insurance nor your insurance broker actually read the policies that are placed. Their is way too much focus on the insurance premium, not what the insurance premium spend actually purchased , which is the most critical piece. An equivalent in the physical world would be renting through AirBNB what you think is waterfront property only to find out you’re overlooking a sewage treatment plant. This is how insurance carriers are getting away with denying claims for patient transfers. They get over because they know your too busy to look at the fine print until it’s too late.

If you are curious, and want a second opinion, call (914) 357-8444or CLICK HERE to stress test your home healthcare agency insurance program BEFORE your education becomes expensive.

SCENARIO :You have an elderly customer who still likes to get out, is not entirely isolated at home. Part of the job description for this customer is that they expect the home health aide to bring them out shopping for groceries, perhaps a doctors appointment or two. Point is the care provided is NOT limited to the 4 walls of the patients home. This creates a whole other risk profile for you the Home Healthcare Agency owner. This additional exposure should be identified up front , when it is , it’s critical that the Agency charges a “risk premium” for the additional INCREASED exposure this increased care provides. If the customer balks at the pricing we recommend you walk. This is a whole different subject and article to be addressed later.

CHALLENGE : When it comes to patient care, and potential negligence claims emanating from that care these should be responded to & financed within the professional liability insurance policy designed specifically for home healthcare agencies . Sadly, many of these types of patient transfers occurring outside the home are not covered. Patient transfers, especially when utilizing an auto are specifically EXCLUDED.

We had a situation where the home health aide took a patient grocery shopping. When they were in the parking lot of the store the home health aide began to load the groceries in the trunk of the car. She negligently did this BEFORE first settling the patient, poor process/ training. The patient lost their balance and fell in the parking lot, shattering their hip.

Within months the home healthcare agency was sued by the patient and their family. Fortunately we understood the exposure up front , were made aware this level of care is being provided , making sure it was properly covered by the professional liability insurance. The claim ultimately settled for $680k.

Unfortunately when we are approached by home health care agencies to evaluate their programs we find their current insurance programs specifically exclude patient transfers outside the 4 walls of the home. The difference between being insured for this exact exposure or NOT is usually 2 words. Which (2) words, where is the intellectual capital of a seasoned risk advisor who knows where to look for those (2) words and negotiate them out of the insurance contract before the loss occurs.

TAKEAWAYS:

Understand your potential exposures. You can’t manage what you don’t know. An experienced Risk Advisor in your space will lead you in a discovery interview process that seeks to understand what customer base is, where your customer base is, levels of service you provide , business model and operations. This is where we identify exposures you may have like the patient transfer outside the home example.

Stress Test Your Current Program : After you have identified as many potential exposures as you can in the above exercise make decisions on how to mitigate or finance these potential exposures.

Remember there are only 4 ways to fund a loss:

Current Operating Cash Flow

Cash Reserves

Loans / Credit Line

Insurance

For most small to mid-sized businesses , insurance is the most cost efficient way to finance future potential losses.

Our recommendation is to open up a dialogue with a RISK ADVISOR and have them do the work for you. Often the service is free of charge. There is no downside in checking your home healthcare agencies insurance program .

One of two outcomes will result:

You checked the program for BOTH coverage terms & pricing ; all seems to be in order. Feel good about that.

You have uncovered deficiencies in your program that decisions need to be made on, &/or you were being over charged for the coverage. Often when we evaluate programs we see BOTH adverse scenarios occurring.

In the last few years we have evaluated hundred’s of home healthcare agency insurance programs. We have found coverage deficiencies & pricing improvement opportunities in 84% of the cases we reviewed. Within that 84% cohort 62% had MAJOR deficiencies that could have resulted in the collapse of the Agency should that particular loss occur.

If you are curious, and want a second opinion, call (914) 357-8444or CLICK HERE to stress test your home healthcare agency insurance program BEFORE your education becomes expensive.

I wouldn’t limit this little nugget to just Home Healthcare Agencies, as most smart run organizations know that efficiently utilizing your resources, deploying effectively, is really what creates competitive separation between you and your competitors.

In a recent Wall Street Journal Article “High Turnover of Home Care Givers Makes Life Precarious” it was revealed that the number one challenge home health agencies face is staffing. The challenge is staff recruiting and staff retention. If your in the home health care space you live this . What you might be missing though is how your largest competitors are winning the staffing war, which translates to more business for them. Can’t you just hear their pitch about how deep their bench , which is major consideration in choosing a home health care agency. Make no mistake about it , attracting and recruiting home health aides is THE competitive war right now.

These best run Agencies are using lucrative signing bonuses with vesting provisions to attract and keep home health aides employed by their home healthcare agencies. They are also increasing pay, and adding benefits to their most valuable, best performing workers. If you have your ear to the ground you may know this too. The question you may be asking yourself is where are they finding the money to do this with so much pressure on margins, especially if your income is capped by medicaide & medi-care.

For most it’s simply not in the budget. The numbers just don’t work, unless you know where to look; INSURANCE. Many of these home health care agencies asked a very simple question; if I can reduce my spend on my current insurance program by 15% to 20% that is a potential large pool of funds that I can then re-allocate into employee comps to attract and retain the best talent, WITHOUT a substantial impact on our budget.

Makes sense, however if it were that easy everyone would be doing that right? This is the differentiator. The home health care agencies that have been successful did not just contact 3 insurance brokers, flipping their loss runs, quoting their insurance programs in hopes of reducing their insurance spend by 15%. Been there, done that. Too much effort for not enough yield.

Wilda Diaz , CEO of Above & Beyond Home Care, based in Clifton N.J. revealed to us her experience.

“We had an idea how much all our open work comp claims were costing us , however we didn’t have the resources , bandwidth or insurance claims knowledge to capture the dollars we suspected were out there. By partnering with the right firm we saw an immediate impact. The savings we were able to harness from focusing on this expensive waste of resources we put towards our recruiting efforts, improving our financial results without increasing our budget”.

Home Healthcare Aide

Instead they reimagined the whole insurance purchase experience. Which would you rather have as the CFO of a Healthcare Agency, 15% savings on your insurance program or 3 to 5 point increase in your profit margin? The question is rhetorical as 3 to 5 points on your profit margin is a far bigger number. We suggest instead of letting the insurance carriers choose who your broker is; (lowest rates win the deal), you look deeper. Incidentally the broker with the lowest rates when you bid your program last just happen to have the “right” carrier in the “right” year.

What these forwarding thinking home health care agencies did was interview (2) competing brokers, the incumbent and one other they thought might be a good fit based on experience within their industry asking them to review their program and give them ideas on how they might approach the account. Naturally premiums due matter, however when these home health care agencies realized how much money they were leaking due to claims THAT became the biggest driver in their decision. The broker that could identify organization pain points, designed a plan to mitigate those pain points to help them reduce current claims reserves, close existing open claims AND future work comp & liability claims proved far more valuable to these home health care agencies.

What most home health care agencies don’t understand is how the industry (carriers & brokers) have a different set of goals than do the home healthcare agencies. When you put claims in what happens to your premiums; they go up! When premiums go up who makes more money; Brokers & Carriers! Who makes less money; home healthcare agencies. This is why their business model doesn’t lean into creating claims efficiencies for home healthcare agencies. Ask yourself , outside of a quarterly claims call rehashing past failures, how are they impacting our future costs? What’s the plan ?

In summary, if you have open work comp or liability claims within your current program, or you have an insurance program without ANY deductibles , often called first dollar plans, you are paying far more for your insurance program than the Home Healthcare Agencies that are using COMP CAREas a risk management platform to increasing their profit margins.

These Agencies understood there was money in them there hills. Reporting a liability claim or work comp claim for their home healthcare agencies was just the beginning of the process, not the end. It took them a year to realize the savings compressing the values on current open claims , which reduced their future insurance premium. They took these funds, put it into a pool, and began to focus on increasing the wages for their BEST workers, paying signing bonuses to recruit new workers which allowed them to take on more clients.

It’s very difficult to increase one expense component significantly and not decrease another within a similar range unless you are willing to sacrifice margin, which most home health care companies cannot .

Keith McNamara is a Home Healthcare Practice Leader for Metropolitan Risk. He can be reached at (914) 357-8444.

Most businesses who purchase commercial general liability insurance have little understanding of how it’s structured and what is important. Instead they focus on the amount of limits offered per occurrence and the premium being charged for those commercial general liability insurance limits for their comparison when making their purchase decision. We are here to tell you those are the last 2 data points ( coverage limit & premium) to consider when evaluating your current liability insurance program. It’s a classic price vs cost conundrum.

Over the next few paragraphs we will break down for you the critical components you should use when evaluating your commercial general liability insurance program. The goal here is not to provide a Master’s Class in understanding all of the nuance with respect to commercial general liability insurance. Instead it’s really to get you to consider engaging a Risk Advisor by clicking here to do the evaluation for you. Often times a RISK ADVISOR will not charge you to do the evaluation .

If the RISK ADVISOR is good at what they do they will first understand how you make your money, who your customers are , where you operate, and importantly the contracts that create both upstream and downstream obligations for your company. Understand, your Commercial Insurance Program is always a trailer , it never leads. It reflects and finances potential future losses more efficiently that using your own operating capital. To properly design ANY commercial insurance program both the broker and the customer need to spend time discussing in detail the operational components and risk profile of the business. Contingent on how , where and who you make your money from will determine this critical exercise. it can be fairly simple to pretty complex. You do the heavy lift once , then tweak it yearly to adjust or iterate as your business evolves.

QUICK TIP :You can tell how good the Risk Advisor is by the questions they ask, the process they put forth to understand your business. If it’s ad-hoc, only takes a few minutes that’s a big red flag. Did they analyze your loss runs, contracts, licensing agreements, laws you may be subject to in operating your business, future goals?

We say insurance is always a trailer because the real purpose of insurance is to transfer a future potential “net income loss” (defined as income you would have had except for a particular event), from YOUR balance sheet to the insurance carriers balance sheet for the lowest premium possible. Here is the key phrase AS MUCH RISK AS POSSIBLE for the LOWEST PREMIUM available. More on that later and why that is so important.

Here is the primer I promised before I went off on a tangent to frame this EXPLAINER.

COMMERCIAL GENERAL LIABILITY INSURANCE : The best way to remember this section; there is a reason it’s called “GENERAL LIABILITY”. The reason, its general (non-specific) , kind of plain vanilla , designed mainly to cover the general public. It is NOT designed to cover for losses involving hiring , firing , management practices for your employees. It is NOT designed to cover your customers for specific errors , omissions , designated professional practices as it relates to the duties you perform.

It’s the most generic form of commercial liability insurance available to a business to insulate them from future 3rd party losses. Commercial General Liability Insurance is designed to cover losses you may be responsible to ,a 3rd party, typically the general public for a loss or injury they may have suffered. Think of a pedestrian that slips and falls outside your retail store. They litigate against you and the building owner. The building owner will have their own commercial general liability insurance as will you. Who pays will be determined by the details of the incident and your lease which covers your business obligations.

If you want to understand what your commercial general liability insurance policy covers start with what it DOESN’T COVER by going right to the EXCLUSIONS section of the policy. There you will uncover how potentially woefully inadequate the coverage truly can be.

Without getting too much into the weeds here let me highlight a few key risks & exposures you may have that will NOT be covered in your commercial general liability policy.

CLAIMS BETWEEN YOU & YOUR EMPLOYEES:

Harassment : Could be sexual, could be gender based, could be you just have a bad egg in your midst that is a bully to their co-workers or subordinates. It’s take very little for an employee to file a harassment complaint with the Department of Labor in your State, which will trigger a very expensive Dept of Labor audit. Worse they could lawyer up as they know or have heard it’s an easy way to make a quick buck. They are right, most of these claims come to some financial settlement where your business pays the employee money instead of expensive litigation.

Wage & Hour : These are hugely expensive to a business. Primarily because the audits are invasive, word spreads to ex-employees who want to be on the gravy train, the cost to defend (Employment Attorneys) are expensive. Finally the settlement, if it’s determined that you did not properly pay overtime or other wage related claims.

Just google WAGE & HOUR lawsuits in your industry to read some of the horror stories. It won’t take long for you to determine that having an employment practices liability policy is essential for the continuity of your business.

These are just (2) quick examples. There are far more, like discrimination. Bottom line you MUST transfer this risk to an insurance carrier for a premium as it’s too expensive to retain.

CLAIMS INVOLVING DIFFERENT TYPES OF SERVICES YOU PERFORM:

Examples here would be services that are technical and requiring licensing, specific training e.t.c. A specific example here might be a home healthcare agency that provides at home services for the elderly. If in their daily routine it’s asserted the home health aide fails in their duties or is negligent, a patient falls breaking their hip, the home healthcare agency may be held liable if they were negligent in their duties resulting in a significant injury. Even if you feel you were not negligent, the cost to defend yourself going to the matt on the suit will be crazy expensive , even if you win. Unless the Home Healthcare Agency purchased PROFESSIONAL LIABILITY INSURANCE , they are funding this very expensive loss themselves. The cost to defend such an event is easily 6 figures, say nothing of the settlement.

Many non-profits perform services for their “clients” that require specialized services that are typically excluded on a commercial general liability insurance policy . They may provide elder care, youth services, counseling, legal services, placement services e.t.c. Much care needs to be taken to properly understand your risk and exposures to loss , then decide if you want to transfer that risk or exposure to insurance carrier for a premium.

Often with non-profits we conduct a simple contract for services audit to understand what services they have been retained to deliver. Then we audit the professional liability policy to check if that exposure was contemplated . In a recent services audit for a local non-profit we determined that the non-profIt , who was providing job placement services for disadvantaged youth , did NOT have the correct coverage for those services. Their Professional Liability policy did not include molestation coverage which could be critical if they placed that youth in a situation that led to an “event”. Just the assertion of the event could wipe out years of operating budget.

In the above example they did purchase Professional Liability coverage however without that audit , understanding their true exposure to loss , there was the potential for catastrophic failure if someone pointed a finger. Too often , without an audit these non-profits or other business organizations learn of the deficiency after they get the claim denied, making their education very expensive.

CLAIMS DUE TO AN ERROR OR OMMISSION :

In many service organizations, failure to perform a certain job function may result in damages to either your customer or the general public. An example might be a construction firm that improperly installed weep holes in the masonry facade of a building. Water built up behind the masonry wall going undetected for a period of time, ultimately resulting in the façade collapsing onto the street below. This actually happen to one of our clients.

Since they purchased Construction Errors & Omission insurance from us the loss defended and the damages covered. Mostly the re-purchase of new materials and labor to install the material as well. Architectural fees, scaffolding, permits e.t.c. were also covered. The cash provided to investigate, defend and ultimately finance the repair was all paid from the construction errors & omissions policy. This had the affect of allowing the business to keep it’s cash flow, budgets and profits in tact. Errors & Omissions Liability Insurance is available to most service businesses, not just construction.

CLAIMS DUE TO A DATA BREACH :

This one can be fairly complex, with lots of potential for errors. Imagine you get an email from a Hacker stating that unless you pay them a ransom, they are going to slowly release all of your customers private information out into the web. Further they will tell your customers where they got the information and that you refused to pay the ransom which is why all their data is exposed. Imagine your a divorce attorney, a child psychologist, a financial advisor.

There are many examples I can give whereby your customers data or your customers systems are hacked due to a virus that may or may not have come from your network. The mere fact someone may point a finger at your company and make the assertion the hack started from an email your company sent is going to be a 6 figure event. Further they can be very, very expensive to defend. In States like NY where they passed the SHIELD ACT the fines alone from a State or Federal government can put you out of business as the fines are well into the 6 figures.

In this situation you need a standalone Cyber Liability Insurance policy.

QUICK TIP :NEVER think you have coverage for Cyber liability just because your carrier added an endorsement onto your policy with a $ 1 mil limit stating they are covering you for a cyber liability event. Those endorsements fall woefully short of giving you proper coverage. They are hollowed out coverage forms that give the false impression you have coverage. This will only come to light when you file the claim , resulting in a denial.

CLAIMS DUE TO A FAILURE TO COMPLY WITH GOVERNMENTAL RULES & REGS:

Sadly most companies aren’t aware that as a private company you have exposure to loss from rules , regs, codes that create obligations for your company for failure to comply. In this situation a Directors & Officers policy will help provide defense and in some cases help pay for the fines, or settlement due to these code infractions.

QUICK TIP : ON PRICING FOR ANY TYPE OF COMMERCIAL LIABILITY INSURANCE POLICY :

Pricing is predicated upon a “BASIS” ; a unit of measurement that the carrier determines best reflects their actuarial tables to determine the probability of a future loss. This is how they arrive at a premium. Some carriers are flexible with the “Basis” , others are not. They use one type of basis for determining the premiums they charge. You should determine up front what is the best possible “BASIS” for your company to yield the lowest possible premium.

Examples of “BASIS” would be :

Payroll

Sales

Units

Square Footage

Contracts

Contingent on the basis chosen the carrier applies a formula to the chosen basis to arrive at the premiums charged. A huge variable in that formula is your company’s loss pic (loss picture). This is the ratio of historical premiums charged versus claims paid out. Essentially , how much profit has your account generated over the previous 5 years based on incurred loss. For more on LOSS PICS , CLICK HERE.

We plan on doing a future piece just on pricing of Commercial General Liability Insurance as it’s way too much to tackle here.

A final thought there are many risks and exposures that a typical commercial general liability insurance policy will disclaim. We cannot stress enough that a thorough evaluation with a qualified RISK ADVISORof how you do business, where you make your money, how you make your money, from who you make your money is the ONLY way to properly insure the risk.

You cannot properly transfer risk or finance risk that hasn’t been indemnified. Further, unless you stress test your insurance program BEFORE a loss occurs you are setting yourself up for a very expensive lesson.

Are you wondering why the renewal for your apartment building insurance for your rental building, Co-op or Condo has gone up by north of 20% ? This little primer might help explain why. The Chinese have a proverb, “may you live in interesting times”. If you’re an owner of commercial or residential real estate, especially in New York or New Jersey this proverb is an understatement. Faced with the double jeopardy challenge of escalating costs up & down your P&L in tandem with local laws capping your ability to raise rents if your units are subject to rent guidelines , finding new strategies to maintain your margins and investment yield is an imperative heading into 1st quarter to 2023. This is meant to be a primer for buyers or commercial insurance in the Metropolitan New York region. We have taken care to organize our executive summary into lines of insurance which makes the most sense.

Commercial Property Insurance :

For rental real estate , co-op’s or condominium buildings located in the metro NY region It’s all about C.O.P.E. ( Construction , Occupancy, Protection Class, Environment). When an underwriter looks at an account these are the buckets they use to organize how they will price your account. Buildings that have invested in their properties in terms of not just aesthetics ,(tenant) upgrades, but building safety & infrastructure enjoy the most competitive pricing & coverage terms. These are the items that carriers look for in the properties they underwrite.

Sprinkler Systems ( Common Areas Good; Fully Sprinklered Best)

Standpipe Systems

2nd Means of Egress .

Twin Parks Fire

Self Closing Fire Doors.

Auditing of Fire Doors

Emergency Lighting / Exit Signs

Hard Wired Smoke Detectors

System to document repairs, maintenance, upgrades.

Upgraded Electrical systems

Water Sensors & Monitors

Boiler Sensors & Monitors

Upgrade Schedule communicating the installation of some of the features noted above.

At Metropolitan Risk we encourage building owners to use our infra-red scanning technology to scan your building for electrical hot spots. This is a smart pro-active initiative that can save the property owner much blood & treasure by preventing an electrical fire loss up front by identifying areas of your building where the electrical system may be failing before a fire results.

The insurance carriers we see that give the owners the most credit for these features are Travelers, GNY, FM Global, CNA, AmRisk. If your building lacks many of these features they still may quote the account contingent on how well the portfolio has performed in relation to it’s COPE.

As you read this and say to yourself, jeez we have most of this stuff, yet our insurance is still increasing; or we are getting cancelled which is puzzling.

Remember when you purchase insurance through an insurance carrier, you are pooling your risk. This means you are getting lumped in with all the other buildings they are insuring. Each year the carriers, through their actuaries set the insurance companies rates based upon the losses the portfolio is incurring AND the cost of re-insurance. For some carriers it’s a double hit as their losses and re-insurance costs increase.

In the last 5 years , property losses are out passing the previous 10. Climate induced impacts are having significant cost impacts on re-insurance costs which get passed down to you the end user buyer. Remember the pooling of risk applies to the insurance carriers, not just the buyer. It’s all part of the cost food chain to transfer risk.

Many insured’s solely think about their buildings and their account performance, however the macros on the economy, portfolio loss performance , and the cost of their re-insurance contracts really dictate the cost of their property insurance. When you purchase insurance you are deeply impacted in a positive and negative way ; the “pooling of the risk”.

COMMERCIAL LIABILITY INSURANCE :

For your rental apartment building , Co-Op Building or Condominium building ,unlike Property Insurance, which is increasing nationwide due to the cost of re-insurance driven mostly by the macros detailed above; liability insurance has much larger disparities market to market, state to state, locality to locality. New York State & New York City is case in point.

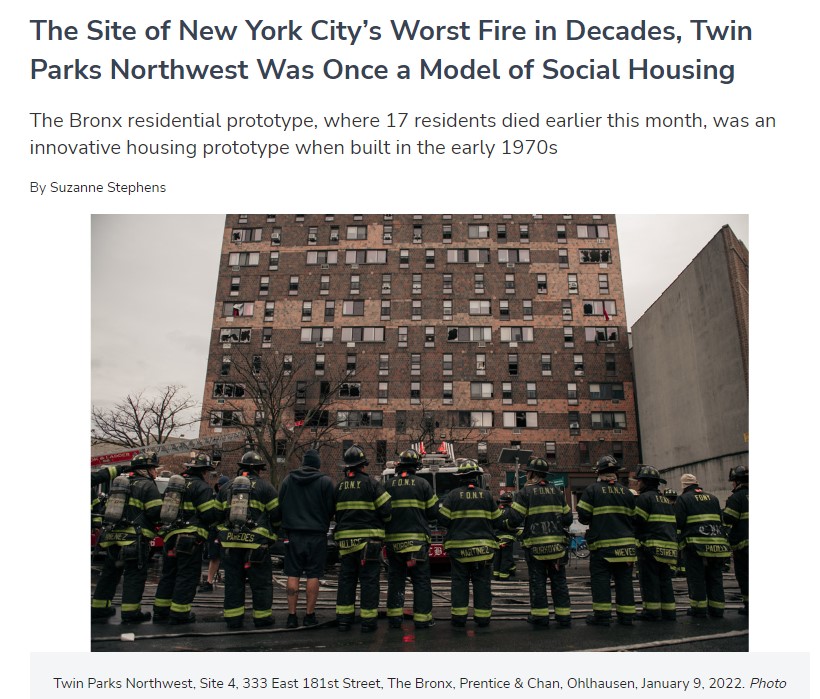

On January 9th, 2022 the Twin Parks Fire sent shock waves through out the New York City Habitational Insurance market; specifically as it relates to liability. In that fire 17 people dies due to smoke inhalation. The 19 story building was rated masonry non-combust which meant it was built primarily with steel and concrete. It had multiple means of egress (ways in & out) , with fire doors protecting the egress. The challenge for the owners and the insurers was the alleged malfunction of the fire door hinges which are self-closing. Due to their alleged malfunction smoke infiltrated the building killing 17 people from smoke inhalation.

What does that have to do with me? Great question; everything. When ever the carriers see a large loss like that come into view they look inward. How many buildings are we insuring that fit that risk profile. The answer was a lot. The determination was made that because the building was NOT fully sprinklered, which would have suppressed the smoke, this type of loss could be inevitable. Thus, the takeaway away for you is that if your building is NOT 100% sprinklered, your rates are going up, by a lot, and many carriers are refusing to insure you as they don’t want a repeat of the TWIN PARKS FIRE.

Sadly, that is only one component of the increase. Due to NY’s Labor Law or the Scaffold Law which imposes strict liability on property owners for workers who fall from a height, payouts on liability claims are significantly higher in New York than almost any other state in the country.

Gallo, Vitucci& Klar who specializes in Labor Law defense. “One of the labor law hotbeds in New York is Lackawanna County in upstate NY, think Buffalo. The Labor Law affects the entire state, not just NYC. That said NYC has a concentration of taller buildings which is why there is more activity there.”

At Metropolitan Risk we wrote an E-Book to help school property owners on the risks inherent in the labor law CLICK HEREto download. For purposes of this article , just understand that the Scaffold Law continues to push insurance costs for property owners much higher in this region than in any other region in the county. Which is a large component as to why your liability insurance costs continue to rise.

EXCESS LIABILITY INSURANCE :

Similar to liability for essentially the same reasons excess liability insurance costs continue to rise with one notable exception.

The DEMISE OF THE “PROGRAM UMBRELLA” : Program Umbrella’s where essentially products where by an MGA “Managing General Agent” would purchase large limits of excess liability coverage , and then turn to retail agents and brokers and give them access to the program for their clients. For a “Premium” the agent or brokers customers could gain access to that particular Umbrella policy purchased by the MGA. Essentially giving real estate owners the ability to purchase at a discount excess liability insurance in “BULK”, getting the “BULK” discount.

As of this time last year there were north of 10 Program Umbrella’s you could bolt into , enjoying liability limits as high a $100 million dollars for your portfolio , or building. Those days are gone. While there are still a few left, the underwriting to get in is uncompromisingly strict, and the pricing discount for buying in bulk is gone.

In over 25 years of serving building owners and developers I cannot recall a more challenging market for this cohort of insurance buyers. There simply is not enough insurance carriers writing this class of risk to drive pricing back down. It’s classic supply & demand. The carriers putting out paper on the street are calling the shots as they don’t have much competition. They are getting their number because the property owners MUST purchase coverage to comply with their lenders requirements. Lender in turn need to understand the dynamics of this current market and work with their property owners to find a balance.

On top of ALL of this are the new unfunded mandates from the City of New York, New York State and the Federal Government for all types of businesses. It’s a very challenging environment to be a landlord in New York City as the income is capped, but the costs continue to escalate higher than the other side of the P&L.

There are strategies building owners can take to mitigate some of these escalations. That is fertile ground for our next article in the series.

We hope you found this piece informative. Feel free to reach out to a Risk Advisor by calling (914) 357-8444 or simply CLICK HERE.

In our opinion, there is no better time to consider alternative risk transfer as a strategy to get more cost-efficient with respect to your current commercial property insurance, commercial liability insurance, workers compensation insurance, & commercial auto insurance.

As I write this the country and the world are about to exit the covid pandemic. If we frame the current conditions in terms of where we are in the property insurance, liability insurance & workers compensation insurance buying cycle; conditions couldn’t be more favorable to give your company a significant competitive advantage.

Taxes :

Since all 3 branches of government have changes hands in the last several years there are strong tailwinds pushing for significant tax increases which will erode corporate resources. We suggest utilizing a Captive Insurance strategy can give you significant tax efficiencies allowing you to keep the dollars inside your company to help reduce your variable cost structure. DOWNLOAD our Guide to Utilizing Captives by CLICKING HERE.

Coverage Availability & Rates :

Currently, we are in the through of a “HARD MARKET”; where conditions favor the insurance carriers as they restrict coverage and increase rates. Insurance buyers are frustrated because they have limited options. Further, they feel squeezed, and rightly so. The carriers are pointing to the “Social Inflation” of liability and commercial auto claims due to the insane jury awards. Buyers are pointing to “profits” earned and surplus growth to counter that claim. We think the buyers have a legit gripe.

Risk As Strategy :

Smart forwarding thinking CFO’s and C-Suite Executives understand that if they can leverage their balance sheets by increasing their retentions EFFICIENTLY, they can gain significant cost advantages that they can bake into their COGS (Cost of Goods & Services). If done properly they can reduce their insurance program costs by 35% which allows them to grow profits, market share, or both. Remember every dollar you save in your insurance program falls directly to the bottom line.

To understand if your company could benefit from a partial or full-on program restructuring CLICK HEREto schedule a 15-minute call. In 5 questions we can figure out if the strategy has legs for your org.

Have you ever wondered how utilizing captives, a high deductible insurance program, alternative risk transfer, self-insured retentions, or retrospective rating plans could further reduce your commercial insurance costs off your already low commercial insurance rates?

Too often business owners are chasing the wrong rabbit. They think that by purchasing their commercial insurance for less than they spent the year before is they accomplished their goal. We get it, it’s an easy benchmark to measure. If you succeed it’s a win; all be it a hollow win unless you really understand what you gave up to get that cheaper price.

Their real goal should be to lower their “Costs”, not the price of their insurance program. Nothing is more expensive to your balance sheet than cheap insurance.

The second huge mistake we see is that although their company has grown, sometimes significantly over the years, they are in essence the same insurance program they were when they were 20 employees; now they are 250, a thousand employees, and yet the commercial insurance is structured in the same way as when they first started.

This is a huge mistake because they are not leveraging their size and scale to reduce their insurance costs. I’m not talking about getting a lower rate because your sales are now at 100 million versus 10 million. That’s actually the illusion the commercial insurance market is selling. They are letting you feel like your reducing costs because of your scale; except they are holding back the best stuff only if you are smart enough to ask. We did a whole piece on the WHY they hold this information back in our “MISALIGNED GOALS” segment. Go there if you want to understand why.

For our purposes focus on the “HOW. First off we are assuming you have strong financials and a solid balance sheet. If you compare your balance sheet today with what it was 20 years ago, it’s probably night and day. Assuming you have solid free cash flow, credit lines, and cash reserves the question becomes, why are we buying so much insurance in the first place? To be clear I’m not talking about insurance limits. That stays the same due to your contractual obligations to your customers and lenders.

Leverage Your Balance Sheet To Reduce Costs At Scale

By leveraging your balance sheet you could restructure your present insurance program to incorporate some “risk-sharing” through higher retentions than by purchasing a “first-dollar plan. In a “first-dollar plan” the insurance carrier funds the loss from the “first dollar”. Any smart CFO worth their salt knows that any insurance coverage accessed for claims is essentially a credit line in reverse, except the interest rate on that credit line is crazy-expensive.

By increasing your retentions you score a lot of runs with one swing of the bat, pardon the baseball analogy. It’s called a grand slam. As your retentions increase the insurance marketplace looks at you entirely different than simply a purchaser of insurance products. You become a “Risk Partner” with them. This is important because the smart insurance carriers know that when you the end-user has “skin in the game” you generate significantly more underwriting profits than those that simply purchase first-dollar insurance plans. For this risk partner relationship, they give you significant discounts off the total premium for your risk sharing. A first dollar or low deductible insurance plan can never discount their rates low enough to get to the risk-sharing discounts.

Retaining Your Risk

Secondly, you purchase less coverage; the same limits, because you’re retaining some of the risks through deductibles or retentions. How you structure that retention matters. That’s another article. You can check out our quick piece on The Difference Between a High Deductible v.s. Self Insured Retention Since you are purchasing less your costs drop far more than just fighting for a lower rate. By taking higher retentions you can lower your costs by magnitude over just getting a lower rate.

Lastly, you can get access to a whole other section of the commercial insurance marketplace that caters to “Alternative Risk Financing” than you would otherwise have access to. You would never see a quote from this marketplace at the lower retention limits because that is not their appetite. They want larger, middle-market companies that want to be risk-sharing partners and not just insurance product providers.

Once you get a taste of what this looks like and how it can benefit you, then you will be tugging at our shirttails for a CAPTIVE STRATEGY.

So if you have been swimming at the same watering hole for years, with the same broker, and the same insurance carriers quoting you every 3 years we suggest you seek a whole new oasis. Call a Risk Advisor today, with 5 simple questions we can test whether this is an option for you.

How much does it cost to start and run a captive insurance company? It’s the most frequent upfront question we get from organizations that are looking at starting their own captive insurance company for their organization. The short answer is zero, but when we tell business this they’re left in shock. After we walk them through the process of how we got zero as the price, it makes perfect sense.

Let’s start at the end and work back; reverse engineer this. First off it’s an investment that yields an ROI, not an expense like your current insurance program. A well-run captive generates has gross savings of at least 30% off your current insurance program on average; irrespective of what structure you’re coming from; unless of course, it’s another captive. That’s because the captive shares in the underwriting profits would typically go 100% to your insurance carrier. Curious about Captives? If you want a better understanding of what a Captive is, and how it could fit in your organization CLICK HERE to download our free ebook.

Further, the risk-sharing mechanism is designed to reduced your upfront premium outlay. Your betting on yourself that your losses will be less than your premium & admin costs. In a well-designed, well-run Captive the results are undeniable. You can only generate & retain these profits, with tax efficiency, in a captive structure. Thus if you back out the cost to run and administer the captive from the profits you generate the cost is ZERO! Someone smart told me years ago that you have to spend money to make money.

In order to consider a captive structure you need these three (3) attributes :

Size & Scale: You need to be spending in excess of $500k in your property & casualty insurance program. You can include employee benefits here too if you wish. Many captives are set up to fund employee health expenses to save on their health & benefits insurance premium. The closer you get to $1 mill in total insurance spend, the better this solution looks. As the numbers you expense in your insurance program increase there is a direct correlation by % to your end benefit.

Free Cash Flow: In finance terms, you need to have strong financials and good free cash flow. The captive will plug into this “resource” and amp it exponentially for your company by keeping that free cash flow tax free instead of it having the direct profits spill down into the partners’ individual tax return.

Underwriting Profits: Too often when we interview companies and CFO’s about a Captive Alternative their main driver is looking for a cheaper insurance quote. They think that by forming a captive they can out run their claims problems and high insurance premiums. This is a fools’ errand. The last thing you want to do is switch places with the insurance carriers if THEY aren’t making money on your account.

Our demarcation line is a minimum of 35% undeveloped loss pic; which is a ratio between incurred claims & premiums paid. If your loss pic is just over that 35% threshold we should have a discussion. If your over 50%, you need to solve your claims problems first before you can consider a captive solution as a potential option.

Breaking Down the Cost of a Captive

You can’t simply compare the “cost” of a captive to the “cost of your current insurance program”, especially in a 1-year snapshot. The correct way to evaluate whether a captive solution is right for your organization purely from a numbers standpoint is a (5) year window. The data set is larger and more representative of your management team. It’s less “noisy” from a numbers standpoint, enabling you to see the big picture.

Further to simply look at this purely in terms of financial implications we suggest is short-sighted as well. This a long-term strategic play. Captives have major strategic advantages as you compete for business on the street than simply buying and expensing insurance year over year.

In our view, Captives are an investment that yields a consistent, measurable ROI, not a cost or expense. It’s an investment in YOU, for YOU! If you want to be at the vanguard and stay 3 steps ahead of your competition we suggest you open up a dialogue of what this solution could look like for you. CLICK HERE to have a 10-minute discussion with one of our Risk Advisors.

With respect to your commercial general liability insurance policy; choosing between a high deductible or self-insured retention can have a major impact on your competitive position as your business competes on the street. We we want to give you some direction BEFORE you pick the insurance program structure for your commercial general liability policy.

Difference Between Self-Insured Retention & Deductible When It Comes To Credit

The first is who is issuing your company “credit”. With a deductible, it’s the insurance company. When a claim needs to be paid out, it’s the insurance carrier that pays the full dollar amount; provided coverage was triggered. The insurance carrier then invoices your company for the agreed-upon deductible amount. Your client (if we are speaking about a liability policy ) is made whole. Thus it’s the insurance companies balance sheet that’s out front, not yours. This is important an important distinction.

With self-insured retention, it’s YOUR companies balance sheet that gets put out front. The reason being; if a claim is presented that needs to get funded YOUR COMPANY pays the claim (up to the retention limit) ; THEN the insurance carrier comes in & funds the remainder of the loss. The point being your customer is issuing you “credit” in hopes that you have the financial capacity to fund the loss.

Difference Between Self-Insured Retention & Deductible When It Comes To Infrastructure

The second big issue is one of infrastructure. When you purchase an insurance policy with a deductible all of the insurance carriers infra-structure comes with it. This may include insurance adjusters, legal representation, engineering & forensics, professional accident investigation e.t.c. An insurance policy that has a deductible structure includes the carrier’s infrastructure for you to leverage.

In a Self Insured retention structure, you must provide the infrastructure. Adjusters, Loss Control Engineers, Legal representation (defense), a professional accident investigation team. At Metropolitan Risk we have all of this pre-built for our clients that choose to leverage the self-insured retention advantage.

Too often we meet the executive team of a company that cannot articulate the strategy of how they ended up in a particular insurance program structure. These companies are backed into their insurance programs because the insurance is the cheapest quote they’ve received. We are brought in because their costs keep rising because they started with the wrong goal. Our clients understand the price they pay on their insurance program is a direct result of how they prevent and manage their claims.

If your main challenge is “frequency” we suggest the self insured retention model. The main reason, you have far more control with a self-insured retention. Since it’s your infrastructure, they work for YOU, not the carrier; it’s your money. Thus you have a degree of control and efficiency that you don’t with a high deductible program. Where we see this being the most successful is where there are a lot of small nuance claims, trip & falls as an example.

Insurance carriers are claims processing factories, they just can’t achieve the same results that our self-insured retention clients can because they handle too much volume to give these small claims the kind of attention they need. Thus our clients that adopt this structure significantly compress their claims.

Those that stay inside a deductible program, or worse a 1st dollar plan (the carriers pay all claims from the first dollar). This is what we call the stealth commercial insurance squeeze. This is where the “incurred” claims continue to rise, resulting in commercial liability insurance premium increases! Remember; commercial insurance is essentially a really expensive credit line. The surcharges on these first dollar plans can result in a death spiral if you don’t take action.

A high deductible program works best in severity issues; (where you have 1 or 2 large claims in a policy year, think LABOR LAW!) No need to build out and pay for infrastructure; incurring those costs if you’re not going to materially impact the ultimate incurred loss which is key to achieving your goal. The more you positively impact your claims results the cost of the entire program reduces which is your goal.

Review your current loss history, run a loss pic, analyze what’s driving the results of your claim. Do you have a “frequency” issue or a “severity” issue? Once you understand your main challenge, then pick the correct insurance program structure to leverage. The best way to improve the results of your claims and lower the ultimate cost of your insurance program is to prevent the losses from happening in the first place.

Call a Risk Advisor today @ (914) 357-8444 or schedule a 10-minute callto walk through your challenge with our team.

Your operations are as a General Contractor, but the contract you are looking to enter (or have entered) references to your organization as a Construction Manager. Is there an issue here?

Although at first glance you may see similarities between a General Contract (“GC”) and Construction Manager (“CM”), their difference in operations, and in turn exposures, are vastly different. Understanding the roles of a General Contractor (“GC”) and Construction Manager (“CM”) and their corresponding interests in a job is important to fully grasp the risk associated with each.

What is a General Contractor and their role?

A General Contractor is typically hired after the owner has a finalized design in place (the design-bid-build model). When bidding on the job, a General Contractor submits complete plans in accordance with the pre-designed specifications. In hiring a General Contractor, the Owner in turn is trusting the General Contractor’s network of employees (direct labor) and subcontractors to perform the work at the job site. The General Contractor will then oversee the day-to-day activity of all direct labor and subcontractors at the job site. The General Contractor’s incentive is to complete the job under budget to maximize their profit.

What is a Construction Manager and their role?

In contrast to a General Contractor, a Construction Manager’s services contract directly with the owner, typically for a fixed fee basis. The Construction Manager’s relationship with the Owner is more of a collaborative/consultative partnership. This brings a different relationship when compared to that of a General Contractor with Ownership since the Construction Manager is usually involved in the project from the start (the design-build model). The Construction Manager has input on the design phase of the project and works directly with the subcontractors during this phase. With this input comes a potential exposure to Professional Liability (E&O).

Defining your organization’s role early in the project is paramount, and a key factor to ensure you are protecting the organization. The contract will be the first place all parties look to when an incident occurs, and you want to be sure that your operations are clearly defined, and within the scope of your insurance coverage.